Today’s Top News & Analysis

Egypt expects Suez Canal revenues to hit USD8.8bn in 2023

Egypt studies a Chinese offer to establish an iron industry complex

Egypt to issue panda bond with a value of USD500mn

A consortium of Orascom Construction and Metito to build USD2.4bn water treatment plant in UAE

HRHO Q1 2023: Astonishing profits

SKPC Q1 2023: Higher prices lead the way

MICH 9M 2022/23: Exceptional y/y veils sluggish sequential performance

EIPICO Q1 2023: Low y/y growth but negative q/q

SUGR Q1 2023: FX gains result in a triple-digit growth in net profits

GEMMA Q1 2023: A new high for margins

MACRO

Egypt expects Suez Canal revenues to hit USD8.8bn in 2023

Chairman of Suez Canal Authority (SCA) said that Egypt expects to record revenues of USD8.8bn (+10% y/y) from ship transit fees in the Suez Canal during 2023 in light of the revenues achieved in the first quarter of this year, which came in at USD2.3bn. (Asharq Business)

Egypt studies a Chinese offer to establish an iron industry complex

Chairman of the General Authority for Suez Canal Economic Zone (SCZone) said that Egypt is studying a Chinese offer from two companies, CDI Sinoma and Sheng Feng, to establish an iron industry complex in SCZone with a total investment of USD300mn. The project will be implemented in two stages, starting with the first phase directly to meet the demand of the local and export markets. (Economy Plus)

Egypt to issue panda bond with a value of USD500mn

The Egyptian government is aiming to issue panda bonds with a total value of USD500mn during the last quarter of this year. (Al-Mal)

Corporate

A consortium of Orascom Construction and Metito to build USD2.4bn water treatment plant in UAE

A consortium of Orascom Construction [ORAS] and Metito will develop, own and operate a large-scale sea water treatment and transportation plant in UAE, in cooperation with with the Abu Dhabi National Oil Company PJSC (ADNOC) and Abu Dhabi National Energy Company PJSC (TAQA). Moreover, the project will be run through a special purpose vehicle (SPV) by a a build, own, operate and transfer (BOOT) model for 30 years, where ADNOC and Taqa will own a 51% stake, while ORAS and Metito will own 49% (24.5% each).

The new USD2.4bn Abu Dhabi project implies USD588mn in new awards attributed to ORAS. This is 19% of ORAS expected 2023 new awards and 11% of its expected 2023 new awards including 50% of BESIX. What is even more interesting about this project is that the (BOOT) model that will result in recurring income for ORAS over the next 30 years. Exact details of how much that is are not yet available.

This confirms our positive view on ORAS which we last updated on 9 April 2023 with a higher 12MPT of EGP215/share. (Company Disclosure)

HRHO Q1 2023: Astonishing profits

· EFG Hermes Holding’s [HRHO] Q1 2023 net income surged 157% y/y to EGP885mn on the back of 129% y/y growth in revenues to EGP4.4bn, mostly dominated by the Investment Bank platform which grew by a staggering 237% y/y to EGP3bn. However, from a quarterly perspective, the top line declined by 4% q/q and the bottom line grew by only 9% q/q.

· The Investment Bank platform strong performance came in as:

o Brokerage revenues increased by 44% y/y to EGP621mn.

o Investment banking segment revenues increased 237% y/y to EGP216mn.

o Direct investment segment grew by 191% y/y to EGP67mn.

· Meanwhile, the NBFS segment growth came a bit tamer, growing by 15% y/y to EGP689mn. Stronger annual performance came due to a massive leap in ValU portfolio and top line, where the consumer finance company recorded top line of EGP254mn (+78% y/y).

· Finally, the commercial banking operations (namely aiBank) saw its bottom line grow 25% y/y to EGP171mn. The bank’s revenues surged by 65% y/y to EGP727mn in Q1 2023.

· We note that HRHO booked FX gains of EGP1.1bn during the quarter and an increase of 537% y/y in revaluation of FI-P&L of EGP705mn. (Company disclosure)

SKPC Q1 2023: Higher prices lead the way

Sidi Kerir Petrochemicals Co. (Sidpec) [SKPC] reported Q1 2023 results, where profits grew to EGP520mn (+107% y/y, +5% q/q) on higher revenues of EGP3.6bn (+71% y/y, +27% q/q) with a 29% GPM (+11pp y/y), driven by:

· Higher prices across all their products, thanks to inflation:

· Exported polyethylene (+54% y/y, +36% q/q).

· Local polyethylene (+64% y/y, +27% q/q).

· Ethylene (+32% y/y, +34% q/q).

· Increased ethylene sales volume (+111% y/y).

· Recording an interest income of EGP62mn (+637% y/y, +54% q/q).

These factors helped offset the decline in:

· Export polyethylene sales volume (-25% y/y, -5% q/q).

· Local polyethylene sales volume (-14% y/y).

· Recording an FX loss of EGP233mn (vs. no FX losses the previous year and only EGP0.76mn the previous quarter).

Furthermore, SKPC’s GPM declined by 2pp q/q as a result of:

· Lower ethylene sales volume (-19% q/q).

· Lower export polyethylene sales volume (-5% q/q).

· Higher processing costs/ton, offsetting the feedstock cost/MMBtu decrease from the new EP cost formula. (Company disclosure)

MICH 9M 2022/23: Exceptional y/y veils sluggish sequential performance

Misr Chemical Industries [MICH] reported its results for 9M 2022/23, recording net profits of EGP435mn (+194% y/y) on higher revenues of EGP676mn (+70% y/y) with a 70% GPM (+16pp y/y), driven by:

· Higher local revenues (+70% y/y) and higher export revenues (+70% y/y).

· FX gains of EGP60mn (+613% y/y).

· Investment income of EGP51mn (+228% y/y).

Meanwhile, the company’s Q3 2022/23 net profits declined with a 12% q/q to EGP155mn on lower revenues of EGP220mn (-14% q/q) with a 68% GPM (-5pp q/q), driven by lower local revenues (-14% q/q) and lower export revenues (-15% q/q) because of decreased demand. (Company disclosure)

EIPICO Q1 2023: Low y/y growth but negative q/q

EIPICO [PHAR] reported Q1 2023 consolidated net profits of EGP188mn (+9% y/y, -17% q/q) on revenues of EGP992mn (+7% y/y, -22% q/q). Meanwhile, the gross profit margin climbed to 49% (+5pp y/y, +12pp q/q), as PHAR managed to decrease its supplies costs by 5% y/y and 30% q/q. (Company disclosure)

SUGR Q1 2023: FX gains result in a triple-digit growth in net profits

Delta Sugar [SUGR] reported its full Q1 2023 results, posting strong net profits of EGP324mn (+321% y/y), due to:

· Higher revenues of EGP775mn (+29% y/y).

· Gross profit margin expanding to 30% (+11pp y/y).

· Huge FX gains of EGP216mn vs. only EGP10mn last year. (Company disclosure)

GEMMA Q1 2023: A new high for margins

Ezz for Ceramics and Porcelain - GEMMA [ECAP] Q1 2023 results show a 22.3% higher net income of EGP57mn compared to EGP46.6mn the year before (5% lower than Prime Research expectations). Revenues grew by 35% y/y to EGP611mn compared to EGP453.8mn the year before (6% lower than Prime Research expectations). Revenues can be broken down into the following:

· Local sales grew by 30% y/y to EGP541.6mn.

· Export sales grew by 85% y/y to EGP69.4mn.

GPM came at a high 35.2% (+8.1pp y/y) on higher selling prices. We think the high margins will normalize over the year, yet still implying the strong pricing power of ECAP. We have an OW/M rating on ECAP with a 12MPT of EGP35.3/share, implying a potential upside of 143%. (Company disclosure)

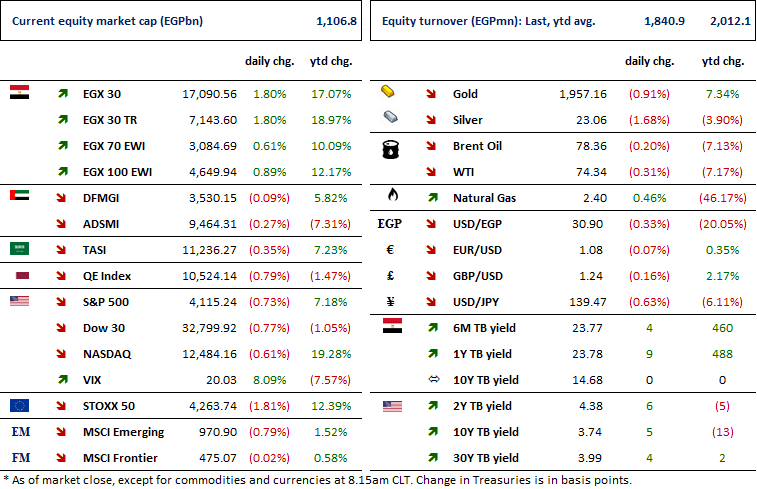

Markets Performance

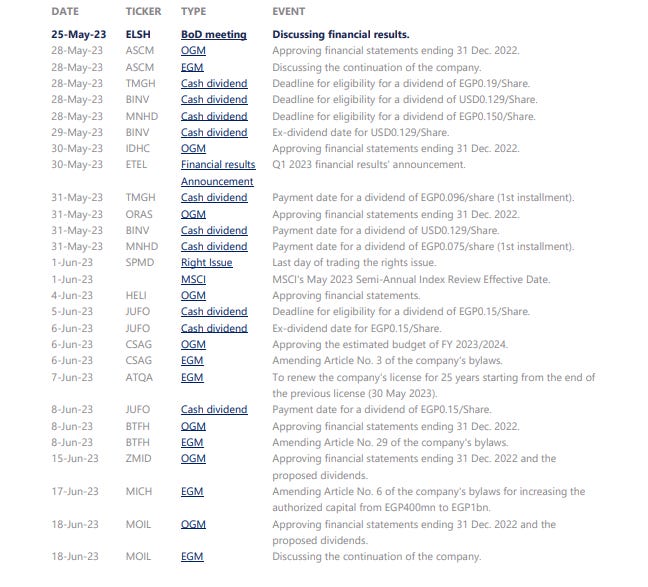

Key Dates

Latest Research