Today’s Trading Playbook

KEY THEMES

B Investments [BINV] has just approved to divest its indirect stake at Giza Systems, amounting to 44.7%. The buyer, STC Solutions, which is a subsidiary of Saudi Telecom Co. (STC), has agreed with BINV to value Giza Systems at an enterprise value of USD145mn. We mentioned before that annual earnings for BINV offer little to be revealed about BINV’s valuation potential. BINV’s most important catalyst, we have stated before, would be the success of a partial or full divestiture of its fundamentally-sound holdings. We have seen favorable response by BINV’s stock price before when the company sold 20% of its stake in Total Egypt. The sale of Giza systems, and the prospect of Ebtikar’s long-awaited IPO, do not really add up to BINV’s market price. BINV is one of the 15 stocks we had picked in our STANDPoint 2022 strategy outlook published on 30 January 2022. BINV is currently traded at 2021 P/E and P/B of 11x and 0.9x, respectively. We have an Overweight rating on BINV, with a 12MPT of EGP16.7/share (ETR +92%).

Elsewhere, Arabian Food Industries (Domty) [DOMT] has received yesterday an acquisition offer from Expedition Investments for up to 90% of DOMT’s total number of shares at EGP5.0/share. DOMT’s stock reacted favorably to the offer, jumping 14% by end of yesterday’s trading session, leaving only 11% upside to the offer price which is a discount to DOMT’s fair value. However, we do not see the offer price as attractive to DOMT’s shareholders. At EGP5.0/share, DOMT is valued at 2021 EV/EBITDA of only 8.7x, given that 2021 was a weak year for DOMT. Hence, we do not believe this to be a deserving valuation to compensate for DOMT’s decent growth outlook. On that note, we believe the offer will be broadly accepted from the market perspective, but it might be revised higher.

These two potential transactions are certainly a proof that Theme #3 in our STANDPoint 2022 strategy outlook is still in play (i.e. M&As). Steeply low valuations serve as a perfect soil for many M&A ideas to blossom.

Now, on to the top news and analysis for the day.

2. Top News & Analysis

MACRO NEWS

The net foreign assets at banking sector witnessed a sharp decline in February, as they fell to negative USD3.29bn against positive USD616mn in January. This is the first negative reading for total NFA since 2017 and also represents a decline for the fifth consecutive month. (CBE)

CORPORATE NEWS

Arabian Food Industries [DOMT] received an acquisition offer up to 90% of its total shares from Expedition Investment at a price of EGP5/share. (Mubasher)

TMG Holding’s [TMGH] OGM approved a DPS of EGP0.17/share (i.e. 2.0% in yield), to be distributed in two installments. (Arab finance)

Palm Hills Development’s [PHDC] OGM approved a DPS of EGP0.10/share (i.e. 6.4% in

yield) to be distributed in two installments. (Arab finance)

Oriental Weavers Carpet’s [ORWE] OGM approved a DPS of EGP1.0/share suggesting a dividend yield of 11%. (Company disclosure)

The Industrial Development Authority decided to conduct the auction for the new cigarette license yesterday, according to the amended conditions booklet, which was announced late last year, amid information that only one company, United Tobacco Morris, a subsidiary of Philip Morris, had submitted for the new license. (Economy Plus)

Madinet Nasr Housing & Development’s [MNHD] second phase capital increase of c.9mn has been fully subscribed. (Arab finance)

Edita Food Industries [EFID] announced the launching of its planet in Morocco, near Casablanca. The facility to be operated by Edita Food Industries Morocco. (Company disclosure)

Telecom Egypt [ETEL] announced the start of operation of the first EG-IX Internet Exchange Center in Egypt, in cooperation with AMS-IX, with the aim of enhancing the digital experience of Internet users in Egypt, Africa and the Middle East. (Arab finance)

Atlas for Investment and Food Industries [AIFI] announced 2021 standalone figures,reporting an 89% y/y decrease in top line of EGP0.681mn (Egyptian exchange)

GLOBAL NEWS

Oil prices inched higher on Monday as worries about tight supply persisted even as investors eyed the release of supplies from strategic reserves from consuming nationsand a truce in Yemen sparked hopes that supply issues in the Middle East could abate. (Reuters)

3. Chart of the Day

Mona Bedeir | Chief Economist

Source: FAO.

The FAO Food Price Index was up by 3.9% m/m in February, 20.7% above its level a year ago. This is a new all-time high, surpassing the previous February 2011 high by 2%. February's increase was sparked by significant increases in the vegetable oil and dairy price sub-indices. Cereal and meat prices increased as well, while the sub-index for sugar prices fell for the third consecutive month.

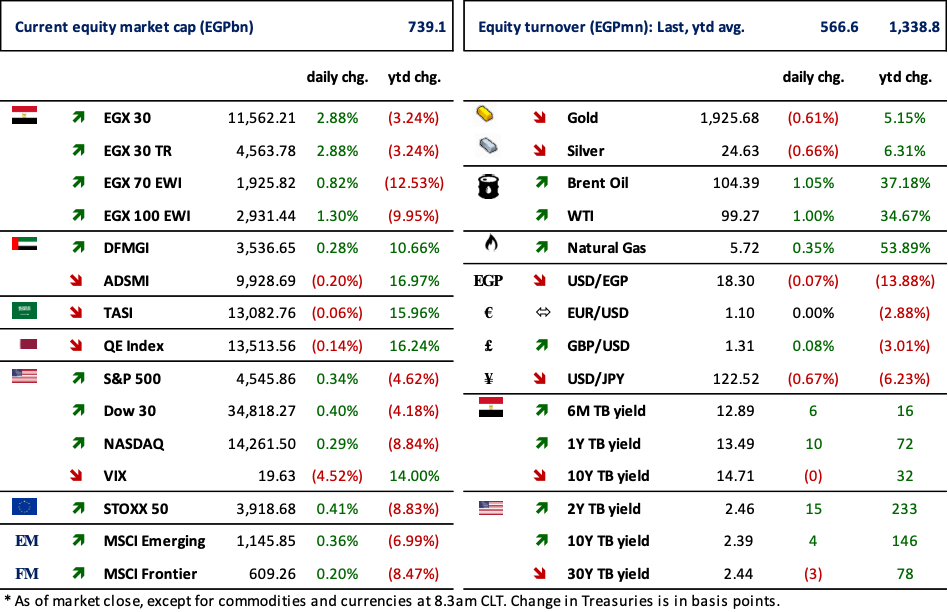

4. Markets Performance