Today’s Top News & Analysis

STANDPoint: The Year of Adjustment; Our fundamental outlook for 2023

Egypt's external debt declined by end of September 2022

GASC launches its second corn tender

Poultry prices expected to stabilize

Obour Land reports record-breaking 2022 results; proposes cash dividends

Abu Qir Fertilizers reports preliminary H1 2022/23 results

Misr Chemical Industries reports its preliminary H1 2022/23 figures

Alexandria Containers reports H1 2022/23 preliminary results

Orascom Development Egypt reports 2022 preliminary results

Qalaa Holding’s BoD approves new ESOP

NBE, CIB ,and aiBank negotiate digital banking solutions with Atos Egypt

A strategic partnership between ISPH and Sandoz Egypt Pharma

FUNDAMENTAL THOUGHTS

STANDPoint: The Year of Adjustment; Our fundamental outlook for 2023

Dear Client,

Last year, 2022, was as eventful as a year can be, not only for Egypt but for the whole world.

Globally, investors had to deal with war where least expected, Europe. Just as the world was on the verge of recovering from a 2-year mayhem resulting from a once-every-100-years pandemic, another global event took us all by surprise on 24 February 2022 when the Russia-Ukraine war broke out. This is almost two years after suffering from COVID-19, further extending global supply chain disruptions and adding another crisis into the mix: energy. All considered we should brace for weaker-than-expected global growth, a gradual fall in inflation rates which will likely continue to be elevated, and less hawkish central banks as they try to accommodate their weakening economies mostly toward H2 2023. Thus, the global investment call by many market pundits has been to overweight fixed-income and underweight equities. Regionally speaking, both emerging markets (EM) fixed-income and equities are in favor as opposed to developed markets, including Europe which is still not out of the woods yet.

Here at home, both local and foreign investors had to deal with two structural events, both relating to the value of the Egyptian pound vs. other hard currencies led by the greenback. Two rounds of EGP devaluation in late March and late October 2022 were enough to turn investors’ attention back to the macroeconomic backdrop. On the one hand, if investors got the macro picture right, they had a better chance of picking the right stocks in the right sectors at hopefully the right time. On the other hand, continued instability means volatile stock returns and hence the importance of following an active strategy.

Taking a closer look at the local market, we notice that all styles ended 2022 in the black, led by value stocks (small-, large-, then mid-cap stocks), which was our call early 2022. Still, growth and core stocks did quite well, generating double-digit returns except for small-cap growth stocks which posted a low single-digit return.

In terms of our factor analysis, it was the highly-liquid stocks that did well (+30%), followed by the liquid stocks (+25%), which were the top performers in 2021, then the illiquid stocks (+22%), the worst performer two years in a row. Also, as we correctly nailed it in 2022, dividend-paying stocks did the trick and returned a good +46% vs. only +11% for non-dividend-paying stocks. Similarly, low-volatility stocks (+31%) outperformed high-volatility stocks (+19%), a switch that we also called for last year. Last but not least, average-beta stocks (+35.5%) outperformed.

But that was last year, what about this year?

We think this year will be the year of adjustment, where investors will need to go back to their drawing boards to devise strategies that deal with more heightened volatility. So, I am not sure why we have to select stocks at the beginning of every calendar year when investing should be throughout all seasons. Thus, this strategy note has our 2023 fundamental outlook, where we lay out our views for Egypt’s macro backdrop, run our equity screens, and lay out our top stock picks in what we would like to consider an “all-weather” portfolio, which we dub as “STANDPoint Portfolio”. This is why we are not making sector-based calls, preferring more of a bottom-up approach.

Wishing you a prosperous year and more years to come.

For the full report, please click here.

—Amr Hussein Elalfy, MBA, CFA | Head of Research

MACRO

Egypt's external debt declined by end of September 2022

Egypt's external debt decreased for the second consecutive month by USD720mn last September to USD155bn. (Economy Plus)

GASC launches its second corn tender

The General Authority for Supply Commodities (GASC) launched a second tender for corn, financed by International Islamic Trade Finance Corporation, with shipping set for 20 February-10 March. (GASC)

Poultry prices expected to stabilize

Poultry prices are expected to stabilize soon due to lower fodder prices (-13% to EGP20,000/ton) and lower soybean prices (-10.5% to EGP25,500/ton). (Al-Borsa)

CORPORATE

Obour Land reports record-breaking 2022 results; proposes cash dividends

Obour Land Food Industries [OLFI] reported 2022 consolidated net profits of EGP462mn (+32% y/y) on higher revenues of EGP4.6bn (+52% y/y):

· Revenue growth was mainly driven by higher prices, where the white cheese average price rose to EGP34.7/kg (+36% y/y) and volumes increased to 123,100 tons (+14% y/y).

· Gross profit margin was pressured down to 21.5% (-2.1pp y/y) due to the EGP devaluation.

Meanwhile, Q4 2022 net profits came in at EGP136mn (+42% y/y) on extraordinary revenues of EGP1.4bn (+61% y/y)—the highest quarterly revenues since 2017, contributing 31% to the total 2022 revenues:

· Q4 2022 revenues grew on higher selling prices, where the white cheese average price grew to EGP42.0/kg (+59% y/y) and sales volumes grew by only 3% y/y to 31,600 tons.

· Q4 2022 gross profit margin rose to 21.1% (+0.6pp y/y) despite the EGP devaluation.

Starting January 2023, OLFI’s management said they saw a massive improvement in USD availability in the banks and, hence they started building back inventory to safe levels. On a related note, OLFI's BoD proposed distributing a cash dividend of EGP0.95/share, implying a 10% yield. Our 12MPT for OLFI is EGP9.2/share, implying a TTM P/E of 5.9x. We will revise our model in view of these results. (Company disclosure: 1, 2)

Abu Qir Fertilizers reports preliminary H1 2022/23 results

Abu Qir Fertilizers’ [ABUK] BoD approved its preliminary H1 2022/23 results, where ABUK recorded a bottom line of EGP7.2bn (+126% y/y) on 80% higher top line of EGP11.2bn and a wider GPM of 65% (+2.2 pp y/y).

Strong annual growth came in view of:

(1) Elevated urea prices.

(2) Weaker EGP, boosting ABUK’s selling prices.

Meanwhile, sequential growth was also strong, where net earnings grew by 59% q/q to EGP4.5bn on 34% q/q higher top line of EGP6.4bn.

On a separate note, ABUK’s BoD decided to postpone the tender related to “Abu Qir III” expansion till further notice as the offers did not meet technical requirements. (Company disclosure)

Misr Chemical Industries reports its preliminary H1 2022/23 figures

Misr Chemical Industries [MICH] reported its preliminary results for H1 2022/23, recording net profits of EGP281mn (+191% y/y) on higher revenues of EGP456mn (+68% y/y). Also, MICH recorded significant quarterly growth in Q2 2022/23, where net profits grew 70% q/q to EGP177mn on higher revenues of EGP258mn (+30% q/q). MICH’s strong performance can be attributed to higher selling prices and FX gains. Furthermore, MICH granted its new hydrogen unit tender to a consortium of EMCCES and UAE-based Gulf Cryo through a Build-Own-Operate (BOO) contract. (Company disclosures: 1, 2)

Alexandria Containers reports H1 2022/23 preliminary results

Alexandria Container & Cargo Handling Co.'s [ALCN] H1 2022/23 preliminary results showed a 151% increase y/y in net profit, reaching EGP1.8bn (39% above our expectations) on revenues of EGP2bn (+78% y/y), exceeding our expectations by 14%. Revenue growth came from handling 379,459 TEUs during the period (6% below our expectations) with an average fee of EGP5,247/TEU (21% above our expectations), mainly due to the EGP devaluation during the period. GPM came in at 76.1% (+11.2pp y/y), the highest in the last five years. On 20 November 2022, we had published a Core Coverage report on ALCN with an Overweight rating and a 12MPT of EGP16.9/share. The stock price has since rallied by more than 54% from EGP13.02/share on 20 November to EGP20.05/share on 29 January 2023, bypassing our price target. (Company disclosure)

Orascom Development Egypt reports 2022 preliminary results

Orascom Development Egypt [ORHD] reported its preliminary 2022 results, where revenues increased 20.7% y/y to EGP11.1bn, a new high for ORHD, compared to EGP9.2bn a year before. The number of units sold slipped slightly by 0.8% to 1,444 units, while the average price increased to EGP38,252/sqm (+24.8% y/y). (Al-Mal)

Qalaa Holding’s BoD approves new ESOP

Qalaa Holding’s [CCAP] BoD approved their new employee stock ownership plan (ESOP), which will allocate 5% of CCAP’s outstanding shares towards stock dividends for employees. The plan will be effective for six years, following final approval from the FRA. (Company disclosure)

NBE, CIB ,and aiBank negotiate digital banking solutions with Atos Egypt

Atos Egypt, a digital transformation leader, announced negotiating with National Bank of Egypt (NBE), Commercial International Bank [COMI], and Arab Investment Bank (aiBank) to set up digital banking services for those banks, similar to Banque Misr’s. (Al-Mal)

A strategic partnership between ISPH and Sandoz Egypt Pharma

Ibnsina Pharma [ISPH] signed a strategic partnership with Sandoz Egypt Pharma to promote and distribute the latter’s over-the-counter (OTC) products. The aim of this partnership is to provide these products to a higher number of underserved patients. (Company disclosure)

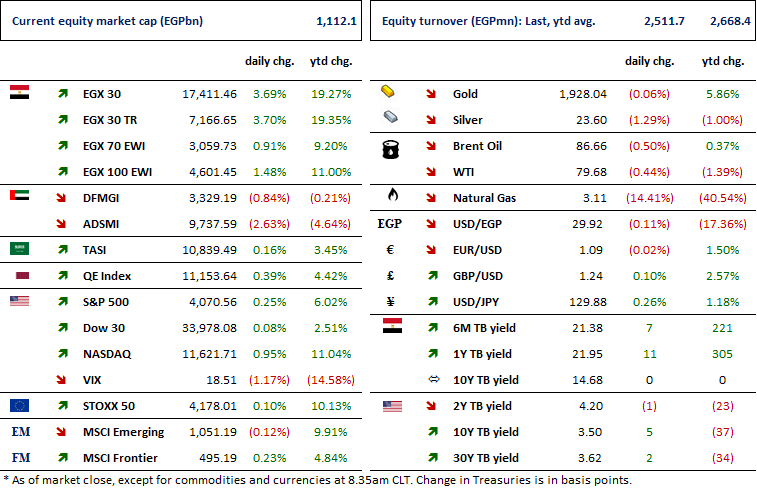

MARKETS PERFORMANCE

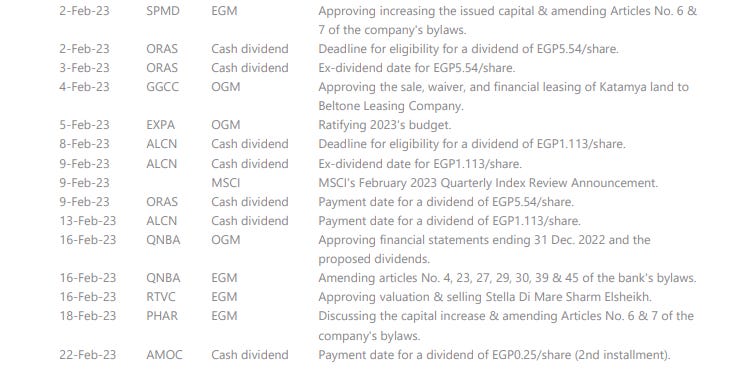

KEY DATES

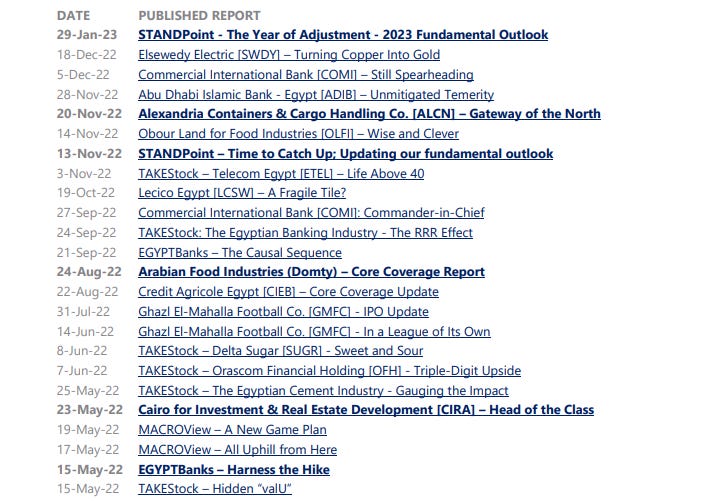

Latest Research