Today’s Top News & Analysis

Damietta Container Handling Co. soon to be listed on the EGX

Elsewedy Electric announces another charged quarterly results

e-finance announced its Q3 2022 results

Fawry disclosed its Q3 2022 results

Abu Qir Fertilizers reports Q1 2022/23

AMOC posts 78% annual growth in its bottom line in Q1 2022/23

EAST announced its preliminary Q1 2022/23 results

Talaat Moustafa announced its preliminary 9M results

Orascom Development Egypt announced its Q3 2022 results

MICH's earnings skyrocketed in Q1 2022/23

CIEB’s Q3 2022 full standalone results

FAIT’s Q3 2022 full standalone results

EXPA reports strong Q3 2022 results

SAUD’s Q3 2022 standalone results

GB Auto announced its Q3 2022 results

Cleopatra Hospitals announced Q3 2022 results

EIPICO announced its Q3 2022 results

Rameda announced its Q3 2022 results

Delta Sugar announced its Q3 2022 results

Edita announced its Q3 2022 results

Domty announced its Q3 2022

Al-Ezz for Ceramics and Porcelain [ECAP] Q3 2022 results

Lecico Egypt Q3 2022 results

AT Lease announced its Q3 2022 results

MACRO

Damietta Container Handling Co. soon to be listed on the EGX

Damietta Container Handling Co. will reportedly have a BoD meeting by the end of the month to discuss the percentage that will be offered to the public on the EGX. We note that Canal Shipping Agencies [CSAG] owns a 20% stake in the company. (Al-Mal)

CORPORATE

Elsewedy Electric announces another charged quarterly results

Elsewedy Electric's [SWDY] Q3 2022 net profits came in at EGP1.2bn (+71% y/y), on revenues of EGP23.6bn (+59% y/y). The revenue mix was as follows:

· EGP11.3bn from the wires & cables segment (+51% y/y), contributing 48% of total sales.

· EGP9.9bn from the turnkey projects segment (+63% y/y), contributing 42% of total sales.

· EGP2.5bn from the other business segments, contributing the remaining 10% of total sales.

· Turnkey projects backlog reached EGP86.9bn (+52% y/y), with EGP20.9bn of new awards during the quarter and EGP36.2bn of new awards during 9M 2022.

GPM reached 13.6% (+1.5pp y/y), supported by the increase in the wires & cables margins which reached 13.5% (+3.7pp y/y). By contrast, GPM for the turnkey segment decreased to 9.2% (-3pp y/y). Other electrical products and renewables segments maintained the highest margins, with 51.4% and 56.3%, respectively.

Net interest expense increased y/y to EGP475.3mn (+202% y/y), with net debt reaching EGP14.8bn. The increase in debt is due to the company's decision to manage its inventory by stockpiling inventory during the rising commodity prices environment. This is apparent in the inventory DOH which increased from 117 days in 9M 2021 to 134 days in 9M 2022, which is an all-time high for SWDY. This helped SWDY lessen the pressure on its margins during the year.

SWDY is one of the 15 stocks we picked in our STANDPoint 2022 strategy outlook published on 30 January 2022. We have an Overweight rating for the name, with a 12MPT of EGP14.3/share. (Company disclosure: 1, 2)

e-finance announced its Q3 2022 results

e-finance's [EFIH] Q3 2022 net earnings skyrocketed by 100% y/y to EGP203mn, owing to a 71% y/y increase in revenues to EGP676mn. The huge top-line growth came on the back of the EFDO segment, which grew by 105% y/y to EGP620mn, coupled with eCards growth by 86% y/y to EGP130mn. Meanwhile, gross profit and net profit margins came in at 58% and 30%, respectively. EFIH is currently trading at an annualized P/E of 34x and a P/BV of 7x. (Company disclosure)

Fawry disclosed its Q3 2022 results

Fawry's [FWRY] Q3 2022 net earnings jumped by 99% y/y to EGP72mn due to the increase in operating revenues by 37% y/y to EGP614mn. Meanwhile, gross profit and net profit margins came in at 61% and 12%, respectively vs. 58% and 8% in Q3 2021. With an annualized ROE of 7%, FWRY is now traded at an annualized P/E of 84x and a P/BV of 6x. (Company disclosure)

Abu Qir Fertilizers reports Q1 2022/23

Abu Qir Fertilizers’ [ABUK] Q1 2022/23 recorded a bottom line of EGP2.8bn (+115% y/y) on an 80% higher top line of EGP4.8bn. Meanwhile, GPM strengthened to 66% (+7.7pp y/y). Strong annual growth came in light of:

(1) Still elevated urea prices.

(2) A weaker EGP, which boosted selling prices for ABUK.

On the other hand, volumes were softer y/y during Q1 2022/23, especially for prilled urea (-5% y/y) and ammonium nitrate (-3% y/y). Meanwhile, sequential growth was also strong. Net earnings grew by 33% q/q, whereas top line upped 12%. We note that Q4 2021/22 witnessed a one-month stoppage in Abu Qir III factory due to annual maintenance, which took place in Q4 2021/22. (Company disclosure)

AMOC posts 78% annual growth in its bottom line in Q1 2022/23

Alexandria Mineral Oils [AMOC] Q1 2021/22 standalone bottom line came at EGP346mn (+78% y/y). Astonishing bottom line performance was sparked by a 60% y/y improvement in the top line of EGP5.85bn. On the other hand, GPM dropped 1pp y/y to GPM to 9%. Massive top-line growth was anchored by (1) improvement in sales volumes by 2.5% and (2) higher average selling prices given the situation in the oil market, besides a weaker EGP. Sequentially, net income dropped 25% q/q in view of a 6% sequential decline in total revenues as well as a weaker GPM. AMOC is currently traded at TTM P/E of 4x. (Company disclosure)

EAST announced its preliminary Q1 2022/23 results

Eastern Company [EAST] reported Q1 2022/23 net profits of EGP1.4bn (-12% y/y) despite a 7% y/y increase in revenues to EGP4.6bn. The decline in net profit is due to lower EBIT at EGP1.9bn (-4% y/y), on higher pension expenses. Meanwhile, gross profit margin expanded to 51% (+6pp y/y). (Company disclosure)

Talaat Moustafa announced its preliminary 9M results

Talaat Moustafa Group Holding [TMGH] reported 9M 2022 consolidated net profits of EGP2.0bn (+15% y/y) on higher revenues of EGP14bn (+23% y/y). GPM decreased to 31% (-2pp y/y). (Company disclosure)

Orascom Development Egypt announced its Q3 2022 results

Orascom Development Egypt [ORHD] reported Q3 2022 consolidated net profits of EGP597mn (+37% y/y). This comes in view of higher revenues to EGP2.9bn (+50% y/y) and a wider GPM of 36% (+4pp y/y). (Company disclosure)

MICH's earnings skyrocketed in Q1 2022/23

Misr Chemical Industries' [MICH] Q1 2022/23 results showed net income growing to EGP104mn (+59% y/y) vs. EGP50mn a year earlier. Stellar earnings growth came in view of (1) a 43% y/y growth in the top line to EGP198mn and (2) a 14pp improvement in GPM to 67%. Revenue growth and GPM improvement were the product of higher average selling prices as caustic soda prices climbed above USD700/ton. MICH is currently traded at 2022/23e P/E of only 4x. We have an Overweight rating on MICH with a 12MPT of EGP20.0/share (ETR +40%). (Company disclosure)

CIEB’s Q3 2022 full standalone results

Credit Agricole- Egypt [CIEB] reported its Q3 2022 standalone full results:

· CIEB achieved bottom line growth of 10% q/q, 45% y/y to EGP586mn. This growth came in light of a 14% q/q, 32% y/y higher Net interest income (NII) of EGP968mn.

· After maintaining a flat growth rate in deposits for the past quarter, the bank managed to significantly grow its pool of deposits this quarter up to EGP54bn, which makes its ytd growth equal to 11%, most of which in this quarter alone.

· CIEB also grew its loan book by 4% q/q to EGP35bn (+14% ytd), with a lower NPL ratio of 2.9% and a higher coverage ratio of 140%.

· The higher coverage ratio is due to higher booked provisions this quarter of EGP61mn (+340% q/q,19% y/y) increasing its annualized CoR to -0.7%.

· CIEB’s NIM is now at 6.7% and an annualized ROE of 24%.

CIEB is now traded at a P/E of 4.5x and a P/BV of 1.1x. We remind you that out 12MPT for CIEB is EGP8.30/share. (Company disclosure)

FAIT’s Q3 2022 full standalone results

FAIT reported its full standalone results of Q3 2022:

· The bank managed to increase its net interest income (NII) by 9% q/q to EGP1bn though it is still 22% lower y/y due to higher Cost of Funds (CoF).

· However, the bottom line decreased 2% q/q to EGP547mn due to: (1) 98% lower dividends income of EGP3mn against EGP132mn in Q2 2022, and (2) booked provisions of -EGP2mn against a reversal of EGP155mn in Q2 2022.

· Other operating income of FAIT’s increased by 200% q/q to EGP219mn by virtue of FX gains as we expected.

· FAIT’s loan book increased again to EGP12bn after it took a strong hit last quarter (+16% q/q, +2.7% ytd) with a NPLs ratio of 1.2% and a coverage ratio of 500%.

· Deposits remained flat for the second quarter in a row at EGP116bn (+0.6% q/q, +6% ytd). The bank’s GLDR now stands at 12%.

With an annualized ROE of 12%, FAIT is now traded at an annualized P/E of 3.2x and a P/BV of 0.5x. (Company disclosure)

EXPA reports strong Q3 2022 results

Export and Development Bank of Egypt [EXPA] reported its Q3 2022 full standalone results. Our main takeaways:

· Although the bank was able to increase its Net Interest Income (NII) by 21% q/q to EGP851mn(+75% y/y) in light of higher yields, however, this increase did not filter through to EXPA’s bottom line that recorded only a 7% q/q increase to EGP338mn (+229% y/y). This was on the back of (1) A much higher effective tax rate of 44% against 32% in Q2 202, and (2) q/q higher booked provisions of EGP85mn.

· On the balance sheet side, EXPA’s loan book increased by 5% q/q, 21% ytd to EGP44bn, with a slightly higher NPL ratio of 3.17% and a lower coverage ratio of exactly 100% which might look a bit alarming.

· As for deposits, which increased only 1% q/q, came at EGP71bn (+10% ytd), pushing the GLDR slightly up to 62%.

EXPA’s NIM is now at 5% and its annualized ROE is at 14%. EXPA is now traded at an annualized P/E of 3.9x and P/BV of 0.5x. (Company disclosure)

SAUD’s Q3 2022 standalone results

Al Baraka Bank – Egypt [SAUD] announced its Q3 2022 full standalone results.

· Regardless of the fact that the bank’s Net interest Income remained flat q/q at EGP887mn, SAUD’s Net income surged by 14% q/q to EGP472mn.

· This was due to three main reasons: (1) 66% lower booked provisions of only EGP38mn. (2) No revaluation losses for financial investments through P&L this quarter against –EGP3mn last quarter (3) A lower effective tax rate of 32% against 34% in June.

· The bank managed to grow its loan portfolio by 8% q/q to EGP27bn, which brings the ytd growth up to 30%.

· SAUD still has a flat ytd growth in its deposits that stands at EGP73bn.

With an annualized ROE of 24%, SAUD is now traded at an annualized P/E of 2x and a P/BV of 0.5x. (Company disclosure)

GB Auto announced its Q3 2022 results

GB Auto [AUTO] reported Q3 2022 net profits of EGP318mn (+71% y/y) despite the 21% decline in revenues to EGP5.1bn. Meanwhile, gross profit margin and EBITDA margin witnessed an increase, coming at 21.4% (+8.3pp y/y) and 13.9% (+6.4pp y/y). (Company disclosure)

Cleopatra Hospitals announced Q3 2022 results

Cleopatra Hospitals [CLHO] reported Q3 2022 net profits of EGP83mn (+3% y/y) on higher revenues of EGP661mn (+6% y/y). (Company disclosure)

EIPICO announced its Q3 2022 results

EIPICO [PHAR] reported Q3 2022 net profits of EGP113mn (+29% y/y) on higher revenues of EGP953mn (+9% y/y). Gross profit margin expanded to 43% (+3pp y/y). On a separate note, PHAR's BoD approved dropping the acquisition of UP Pharma. In addition, PHAR will increase its paid-in capital by 15% to EGP1.14bn at fair value which is yet to be determined by an IFA. (Company disclosures: 1, 2)

Rameda announced its Q3 2022 results

Rameda [RMDA] reported Q3 2022 consolidated net profits of EGP71mn (+56% y/y) on higher revenues of EGP382mn (+21% y/y). Revenues grew despite lower sales volumes to 12.2mn units (-19% y/y). Gross profit margin and EBITDA margin increased to 51% (+4.7pp y/y) and 33% (+7.6pp y/y), respectively. (Company disclosure)

Delta Sugar announced its Q3 2022 results

Delta Sugar [SUGR] reported Q3 2022 consolidated net profits of EGP191mn (+182% y/y) despite the 54% y/y decrease in its top line. Meanwhile, GPM increased to 29% (+25pp y/y). (Company disclosure)

Edita announced its Q3 2022 results

Edita Food Industries [EFID] reported Q3 2022 consolidated net profits of EGP287mn (+154% y/y), on higher revenues of EGP2.0bn (+45% y/y). The huge growth is on the back of higher overall prices, in addition to the increased sales volumes of cake's segment in specific to 610mn packs (+44% y/y). Meanwhile, gross profit margin and EBITDA margin came in at 34% (+4pp y/y) and 22% (+7pp y/y), respectively. Besides an improvement in SG&A-to-revenues ratio have taken place at 15% (-3pp y/y). (Company disclosure)

Domty announced its Q3 2022

Arabian Food Industries [DOMT] reported Q3 2022 consolidated net profits of EGP51mn (-2% y/y), despite a 38% y/y increase in revenues to EGP1.3bn. Meanwhile, gross profit margin came in at 15% (-8pp y/y). Our 12MPT for DOMT is EGP8.7/share and our TTM P/E for is 10.4x. (Company disclosure)

Al-Ezz for Ceramics and Porcelain [ECAP] Q3 2022 results

Al-Ezz Ceramics & Porcelain - GEMMA [ECAP] announced its consolidated Q3 2022 results, where revenues grew to EGP487.6mn compared to EGP357.8mn in Q3 2021 (+36% y/y). Bottom line achieved EGP54.5mn this quarter compared to EGP31mn in Q3 2021 (+76% y/y). GPM decreased slightly from 29.6% to 27.7% (-1.9pp y/y), while NPM increased to 11.2% (+2.6pp y/y). Local sales in this quarter contributed 91.1% of total sales. We have an Overweight rating for the name with a 12MPT of EGP20/share, implying a 72% upside. (Company disclosure)

Lecico Egypt Q3 2022 results

Lecico Egypt’s [LCSW] Q3 2022 net loss came in at EGP9.4mn, compared to a net loss of EGP8.7mn in Q3 2021. Revenues came in at EGP854.6mn (+26% y/y); however, GPM dropped to 13.3% (-5.1pp y/y). The revenue mix was as follows:

· Sanitary ware segment sales contributed almost 60% of total sales, growing by 19% y/y, despite volumes decreasing slightly by 3%. The average price per piece for the segment increased by 22.3% to EGP405/piece, powered by a weaker EGP and high export volumes. GPM for the segment decreased by 9.5pp y/y to a 5%. Exports contributed 75.7% of segment sales, which should bode well for the company in Q4 2022 after the latest EGP depreciation.

· Tiles segment sales contributed 34.6% of total sales, growing by 41% y/y. The increase in tiles sales is attributable to a 25% increase in volumes sold as well as a 13% higher average price per piece of EGP47.6/piece. GPM for the segment increased by 0.5pp y/y to 22.3%.

· Brassware segment contributed the remaining 5.4% of total sales, growing by 18% y/y. The increase in brassware sales is attributable to a slight increase of 3% in volumes sold and the increase in average price per piece by 15% to EGP1,062/piece. The segment’s GPM is still the highest among other segments, with a GPM of 46.7% (+4.8 pp y/y).

Finance income reached EGP149.7mn due to a one-off, while financing expenses came at EGP47.2mn. The increase in financing expense is due to the rising interest rate environment and the increase in LCSW's total debt, which reached EGP1,120mn in Q3 2022.

We have an Underweight rating on the name, with a 12MPT of EGP4.3/share. (Company disclosure)

AT Lease announced its Q3 2022 results

AT Lease's [ATLC] Q3 2022 net earnings fell by 20% y/y to EGP17mn, owing to a drop in the operating revenues by 31% y/y to EGP99mn. Meanwhile, ATLC was able to lower its direct financing expense by 42% y/y to EGP53mn in Q3 2022, leading to a higher gross profit margin of 46% vs. 36% a year earlier. (Company disclosure)

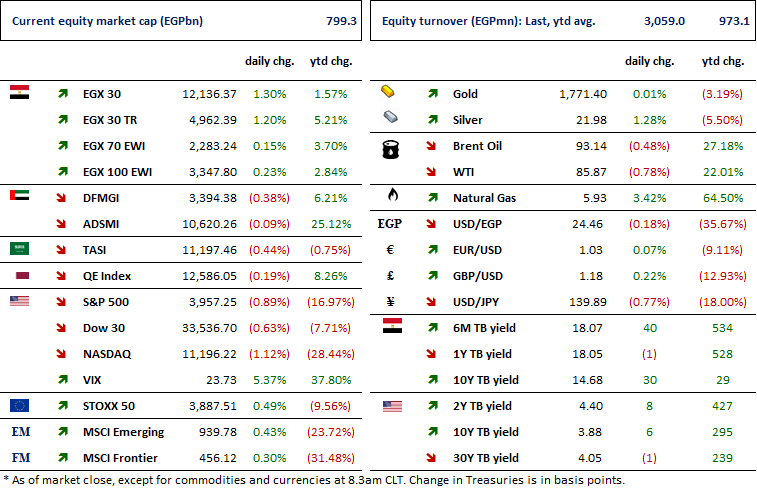

MARKETS PERFORMANCE

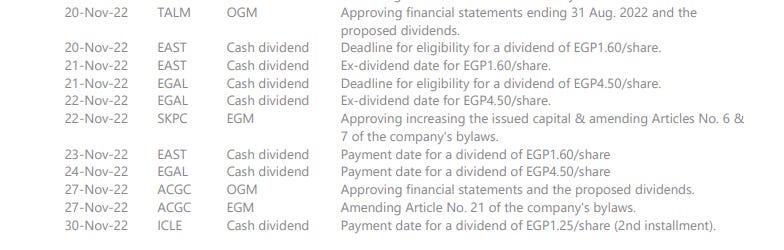

KEY DATES

Latest Research