Today’s Top News & Analysis

Reduced licensing fees for the natural gas sector

Fuel subsidies in H1 FY23 reached EGP66bn

GASC launches Russian wheat tender

Egypt to issue Panda bonds soon

EKHO’s 2022: Strong y/y growth despite a weak Q4; DPS approved; investments pledged

GEMMA’s 2022: Higher margins pushed profits higher

Arabian Cement’s 2022: Higher selling prices strengthen bottom line profits

SKPC’s BoD approves EGP0.5 DPS

Orascom Construction in negotiations to build renewable energy projects worth USD3bn

MACRO

Reduced licensing fees for the natural gas sector

The Gas Regulatory Authority announced new reduced licensing fees for the natural gas sector. The new fees will help encourage investors to continue and even expand their operations in the sector. The new fees are:

· 0.0367 cent/MMBTu (-37% y/y) for transmission.

· 0.0291 cent/MMBTu (-32% y/y) for shipping.

· 0.022 cent/MMBTu (-33% y/y) for distribution.

· 0.009 cent/MMBTu (-31% y/y) for supplying.

· 0.2259 cent/MMBTu (-10% y/y) for compression facility operation.

· 0.2082 cent/MMBTu (-17% y/y) for off-grid transmission system operation. (Al-Mal, GASREG)

Fuel subsidies in H1 FY23 reached EGP66bn

Egypt recorded EGP66bn (+288% y/y) in fuel subsidies in H1 FY23, driven by rising crude oil prices and the EGP devaluation. (Asharq Business)

GASC launches Russian wheat tender

The General Authority for Supply Commodities (GASC) signed a contract to purchase 240,000 tons of Russian wheat for April delivery, financed by The World Bank. (GASC)

Egypt to issue Panda bonds soon

The Egyptian government is aiming to issue USD500mn in Panda bonds by early fiscal year 2023/2024, according to governmental sources. (Economy Plus)

CORPORATE

EKHO’s 2022: Strong y/y growth despite a weak Q4; DPS approved; investments pledged

Egypt Kuwait Holding Co. [EKHO] released its 2022 results, posting net income of USD241mn (+41% y/y) on higher revenues of USD1bn (+37% y/y) with a 45% GPM (+6pp y/y), driven by:

(1) Higher fertilizer gross profit of USD279mn (+123% y/y) on higher revenues of USD486mn (+73% y/y), attributable to Alexfert:

· Greater exported urea sales of USD350mn (+93% y/y), exported ammonium sulphate sales reaching USD58mn (+178 y/y), and exported ammonia sales of USD6mn (+20% y/y).

· Higher export selling prices as a result of higher commodity prices: urea USD698/ton (+76% y/y), ammonia USD1,105/ton (+112% y/y), and ammonium sulphate USD490/ton (+104% y/y).

· Greater export volumes: urea 500,629 tons (+10% y/y) and ammonium sulphate 117,915 tons (+37% y/y).

(2) Higher drilling and petroleum gross profit of USD76mn (+41% y/y) on higher revenues of USD136mn (+45% y/y), attributable to Off Shore Sinai (ONS):

· Lower costs of USD1.9/MMSCFG (-15% y/y).

· Higher prices of USD5.9/MMSCFG (+2% y/y) as a result of higher commodity prices.

· Greater natural gas extraction quantities of 10.3mn MMSCFG (+2% y/y).

(3) Higher chemicals revenues of USD207mn (+21% y/y), attributable to Sprea Misr:

· Higher blended selling prices of USD64/ton (+17% y/y).

· Greater sales volume of 3mn tons (+3% y/y).

(4) FX gains of USD22mn vs. an FX loss of USD1mn a year before.

(5) Higher other income of USD23mn (+266% y/y) and higher interest income of USD9mn (+99% y/y).

However, EKHO posted lackluster Q4 2022 results, posting net income USD34mn (-47% q/q) on lower revenues of USD243 (-7% q/q) and a 29% GPM (-20pp q/q), driven by:

(1) Lower fertilizer gross profit of USD48mn (-33% q/q) on revenues of USD106mn (-14% q/q), attributable to Alexfert:

· Lower revenues of USD106mn (-14% q/q) due to both lower local (-16% q/q) and export (-14% q/q) sales.

· Lower selling prices: Local and export urea prices decreased 15% q/q and 9% q/q, and local and export ammonium sulphate prices decreased 16% q/q and 5% q/q, respectively.

· Higher blended cost of USD273/ton (+21% q/q).

· Lower sales volume of 210,576 tons (-6% q/q) as a result of selling only 22,360 tons of ammonium sulphate (-49% q/q) and not exporting any ammonia in Q4 vs. 3,500 tons sold in Q3 2022.

(2) Recording a chemicals gross loss of (USD7mn) (-146% q/q), attributable to Sprea Misr:

· Lower blended selling prices of USD50/ton (-25% q/q).

· Higher COGS of USD42mn (+29% q/q) as a result of higher raw material costs of USD43/ton (+2% q/q), due to the EGP devaluation.

(3) Lower drilling and petroleum gross profit of USD11mn (-46% q/q), attributable to ONS:

· Lower prices of USD5.7/MMSCFG (-2% q/q), as result of falling natural gas prices.

· Higher COGS of USD6mn (+70% q/q) due to higher costs of USD2.1/MMSCFG (+27% q/q) as a result of the EGP devaluation.

Our net income projections for EKHO were roughly in line with the actual results; we correctly predicted Alexfert and ONS’ net income, but our projections for Sprea Misr and NAT Energy were off by 15% and 17%, respectively.

Furthermore, EKHO’s BoD approved distributing a cash dividend of USD0.11/share, implying a 51% payout ratio and an 8.8% yield for EKHO and 9.9% for EKHOA. The decision is pending OGM approval.

Lastly, EKHO pledged to invest USD170mn during 2023, as follows:

(1) USD50mn to drill two wells in North Sinai for ONS.

(2) USD30mn to complete Nilewood’s factory.

(3) USD11mn to add 20MW to Kahraba’s electricity generation capacity.

(4) USD79mn to purchase minority interest in subsidiaries. (Company disclosures: 1, 2, 3)

EKHO — Rating: OW / M, 12MPT: EGP56.8/share – USD1.9/share (29-Jan-2023)

GEMMA’s 2022: Higher margins pushed profits higher

Al-Ezz for Ceramics & Porcelain’s (GEMMA) [ECAP] 2022 net income rose 60% y/y to EGP171mn compared to EGP107mn the year before as revenues grew by 35% y/y to EGP1.9bn compared to EGP1.4bn the year before. The growth is attributable to the following:

· Local sales grew by 40% y/y to EGP1.7bn, powered by:

o a 29% y/y higher sales volume of 12.4mn sqm of tiles, and

o a 9% higher average selling price of EGP137.6/sqm.

· Export sales grew by 2% y/y to EGP188mn, powered by:

o a 24% higher average selling price of EGP92.8/sqm.

o This was offset by an 18% y/y lower sales volume of 2mn sqm of tiles.

GPM came in at 26.4% (-3.5pp y/y) on a higher raw materials cost and energy costs linked to the USD. (Company disclosure)

Arabian Cement’s 2022: Higher selling prices strengthen bottom line profits

Arabian Cement’s [ARCC] 2022 net profits grew almost tenfold to EGP359mn compared to EGP34.2mn the year before. Revenues grew 91% to EGP4.7bn, which can be broken into:

· Local sales growing by 86% to EGP3.8bn from selling 3.6mn tons of cement and clinker (+22.3% y/y) with an average blended selling price of EGP1,074/ton (+51% y/y).

· Export sales growing by 181% to EGP667.5mn from selling 1mn tons of cement and clinker (+102% y/y) with an average price of EGP666/ton (+39% y/y).

GPM came in at 18.9% (+12.1pp y/y) despite the 83% higher cost of raw materials and energy. The higher GPM is attributable to the great repricing of cement products during the year. The average price per ton of cement for retail customers hovered around USD83/ton in Q1 2022. Prices now average USD66/ton (-20% y/y), albeit increasing c.49% y/y in EGP terms.

In related news, ARCC’s BoD decided not to pay cash dividends for 2022. (Company disclosures: 1, 2)

SKPC’s BoD approves EGP0.5 DPS

Sidi Kerir Petrochemicals Co.’s (Sidpec) [SKPC] BoD approved distributing a cash dividend of EGP0.5/share, implying a 30.5% payout ratio and a 2.9% yield. The decision is pending OGM approval on 21 March 2023. (Company disclosure)

Orascom Construction in negotiations to build renewable energy projects worth USD3bn

Orascom Construction [ORAS] is currently in negotiations with the Ministry of Electricity & Renewable Energy to build multiple renewable energy projects worth USD3bn, which is to be operational by 2028. (Economy Plus)

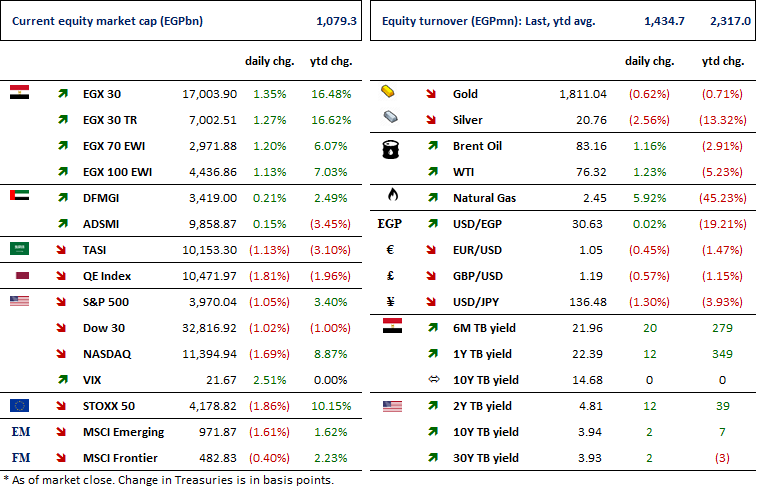

MARKETS PERFORMANCE

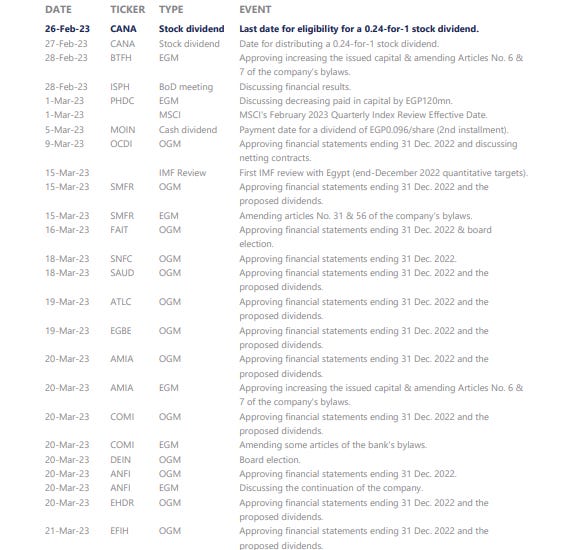

KEY DATES

Latest Research