NEW RESEARCH

Commercial International Bank [COMI] – Coping Mechanisms

The fact that Commercial International Bank – Egypt [COMI] is the largest private-sector bank in Egypt comes at a high cost, just like it comes with benefits. The bank had to be the first to make several changes in its strategy to cope with market conditions, launching new products at a high cost to fend off fierce competition. In turn, other private-sector banks followed suit, which changed the whole sector’s dynamics. However, the distinction here is that these changes, which are usually negative for any bank, only made COMI stronger. Indeed, COMI already had enough space and flexibility to withstand the market conditions and even make the best out of it. This confirms COMI’s strength and leadership in such a volatile economic environment. That said, we update our valuation for COMI, raising our 12MPT by 9% to EGP59.4/share but downgrading our rating to Neutral / Medium Risk.

We up our 12MPT by 9% to EGP59.4/share yet downgrade our rating to N/M: Our residual income-based fair value came out as EGP52.2/share, assuming a long-term ROE of 23% and a terminal COE of 15%. However, we set our 12MPT at EGP59.4/share based on a historical average P/E of 8.5x applied to 2023e earnings. This offers an upside potential of 15%, which is still lower than COMI’s COE. Hence, we downgrade our rating from Overweight to Neutral with the same Medium Risk. Our new 12MPT implies a 2023e P/BV of 2.1x.

Key catalysts: Higher-than-anticipated corporate lending with improving economic conditions. Higher-than-expected earnings growth.

Key risks: Persisting competition from state-owned banks affecting COMI’s deposits. Deterioration in asset quality.

For the full report, please click here.

Today’s Top News & Analysis

Egypt's first gold fund launched

A new USD450mm methanol plant in Damietta

New fuel stations for ships in Egyptian ports

CIB Q1 2023: Reaching new heights

CCAP 2022: Still in the red despite solid revenue growth

ADIB Q1 2023: Exceptional on all fronts

Credit Agricole – Egypt Q1 2023 preliminary: Beyond expectations

Orascom Development Egypt Q1 2023: Higher revenues, yet lower net income

MOIL’s EGM ratifies Al Gihaz offer

MACRO

Egypt's first gold fund launched

The Financial Regulatory Authority (FRA) announced the launch of Egypt's first gold fund which will invest in 24-karat gold, carry no minimum nor maximum investments, and allow investors to fully or partially redeem their certificates either in cash or a minimum of 50 grams of gold. (FRA)

A new USD450mm methanol plant in Damietta

Alexandria National Refining & Petrochemicals Company (ANRPC) signed an agreement with the Norwegian Scatec to build an USD450mn green methanol plant in Damietta. The plant will produce up to 200,000 tons of green methanol per year. (Ministry of Oil)

New fuel stations for ships in Egyptian ports

The Egyptian government grants Minerva Marine the first license to supply ships with fuel in Egyptian ports. Minerva Marine is expected to start its first operations in Port Said Port. (CNBC Arabia)

Corporate

CIB Q1 2023: Reaching new heights

Commercial International bank [COMI] announced its full results for Q1 2023. Below are our main takeaways:

• Net income broke the quarterly earnings record of Q3, by increasing 55% q/q and 44% y/y to EGP6bn.

• This was on the back of a 19% q/q increase (+64% y/y) in net interest income (NII) to EGP10.8bn, which in turn pushed annualized NIM up to 7.5%.

• Net fees and commissions also increased by 35% q/q to EGP1.2bn, while net trading income increased to EGP1.8bn (+158% y/y. +41% q/q), which wiped the effect of the 18% increase in other operating expenses to EGP1.9bn.

• As for provisions, although the booked credit provisions were 24% lower q/q at EGP948mn, they came much higher on a y/y basis against a reversal of EGP41mn in Q1 2022. This implied an annualized cost of risk to 0.4%.

• Loan book surged by 11% ytd to EGP243bn, mainly driven by corporate loans. As expected, NPLs upped a notch to 5.2%, and coverage ratio increased to 233%.

• Despite the 4% ytd decrease in total financial investments to EGP228bn, we can see the reclassification from FI-OCI to FI-AC.

• On the deposits side, growth was 8% ytd to EGP574bn, with GLDR maintained at 42%.

• Annualized ROAE is now up to 39% vs. 23% the previous quarter.

COMI is now traded at an annualized P/E of 8.6x and a P/BV of 2.5x. We remind our clients that our latest 12MPT for COMI is EGP59.4/share, with a Neutral / Medium Risk rating. (Bank disclosure)

CCAP 2022: Still in the red despite solid revenue growth

Qalaa Holdings [CCAP] released its 2022 financial statements, showing a net loss of EGP2.3bn (consistent will last year's numbers) despite revenues growing 113% y/y to EGP97.7bn and GPM expanding 23pp y/y to 35%.

The main drivers for the recorded net loss:

• FX losses of EGP4.7bn (vs. FX gains of EGP228mn in 2021), mainly coming from ASEC Holding (a 69% stake) in the cement segment with EGP3.2bn as a result of the company's Sudanese manufacturing facility and the volatile EGP/SDG FX rate.

• A 26% y/y increase in finance costs to EGP5.5bn due to higher borrowing costs.

Meanwhile, the company's standalone statements showed an impairment charge in loans to subsidiaries of EGP1.1bn.

During Q4 2022 the company suffered most of its losses, posting a net loss of EGP2.1bn (vs. net profits of EGP16.7mn in Q3) despite revenues growing 26% q/q to EGP28bn and GPM staying consistent at 39%. The main driver for the significant sequential loss was FX losses of EGP3.2bn (vs. FX losses of EGP236mn in Q3 2022).

The Egyptian Refining Company (ERC) (a 13% stake), CCAP’s main revenue contributor (c.76%), was the main driver behind the strong revenue growth for the year, supported by substantial margins courtesy of higher petroleum selling prices, which helped improve refiner margins to average USD4.9mn/day in Q4 2022 vs. USD1.8mn/day in Q4 2021). We also note that ERC's receivables from the Egyptian General Petroleum Corporation (EGPC) reached USD618.2mn as of 31 December 2022. Furthermore, CCAP is committed to adding new sources of revenue, mainly medium-sized, export-driven, and primarily environmentally friendly. (Company disclosure:1, 2)

ADIB Q1 2023: Exceptional on all fronts

Abu Dhabi Islamic Bank – Egypt [ADIB] announced remarkable results for Q1 2023. Below are our main takeaways:

• Net income came at EGP968mn (+66% q/q, +129% y/y), marking a new record for quarterly earnings.

• This was mainly due a 34% q/q increase in net interest income (NII) to EGP1.8bn (+76% y/y), which reflects the cumulative effect of the several rate hikes in 2022 and the first quarter of 2023. Accordingly, ADIB’s annualized NIM expanded to 6.7%, up from 5.4% in the previous quarter.

• Annualized cost of risk (CoR) declined to -1.1%, as credit provisions decreased to EGP177mn (-61% q/q). This has allowed the bank to absorb the increase in other operating expenses to EGP276mn due to limited FX losses this quarter.

• On the balance sheet side, ADIB managed to increase its loan book by 7% ytd to EGP63.8bn. Despite this increase, NPL ratio declined to 1.8% and coverage ratio increased to 269%.

• Deposits increased by 4% ytd to EGP102bn, with GLDR ratio up to 63%.

• Although total financial investments declined to EGP23bn (-24% ytd), due from banks increased by 84% ytd to EGP26bn, pushing total assets to EGP124bn (+8% ytd).

• Annualized ROAE skyrocketed to 41% in Q1 2023 vs. 28% in 2022. We note that ADIB have always produced the highest ROAE margin among peers. However, it was usually associated with higher risk. With CAR increasing to 15% and the equity multiplier down to 12.1x, the bank’s higher income is now even crowned by less risk.

ADIB is now traded at an annualized P/E of 3.5x and a P/BV of 0.9x. We remind clients that our 12MPT for ADIB is EGP27.4/Share, rating Overweight/Medium Risk. (Bank disclosure)

Credit Agricole – Egypt Q1 2023 preliminary: Beyond expectations

Credit Agricole – Egypt [CIEB] announced the preliminary results for Q1 2023. Net income took a leap to EGP1.2bn (+150% y/y, +50% q/q), which was partially on the back of a 94% y/y (+24% q/q) increase in net interest income (NII) to EGP1.5bn. Although the bank managed to grow its deposits by 12% ytd to EGP68bn, loan book growth came a lot tamer at only 2.5% ytd to EGP36bn, decreasing the GLDR to 53%. CIEB’s annualized ROAE for Q1 2023 surged to 46% from 33% in the previous quarter. CIEB is now traded at an annualized P/E of 4x and a P/BV of 1.2x. (Bank disclosure)

Orascom Development Egypt Q1 2023: Higher revenues, yet lower net income

Orascom Development Egypt’s [ORHD] Q1 2023 results show net profits shrinking by 31% y/y to EGP291.5mn despite revenues growing by 53% to EGP2.95bn. Revenues can be broken down into the following:

• Hotel revenues grew 120% y/y to EGP573mn.

• Real estate revenues grew 44% y/y to EGP2.01bn.

• Town management revenues grew 32.5% y/y to EGP366mn.

GPM came in at 37.1% (+1.8pp y/y). The lower net income is attributable to an EGP519.5mn loss on the income statement, EGP478mn of which came in FX losses, along with a 180% higher financing cost of EGP210mn. (Company disclosure)

MOIL’s EGM ratifies Al Gihaz offer

Maridive & Oil Services’ [MOIL] EGM ratified Al Gihaz Holding’s offer presented to MOIL’s wholly-owned subsidiary Valentine Maritime Ltd. We had reported on 10 May 2023 that MOIL’s BoD approved Al Gihaz’s final offer worth USD115.6mn for Valentine’s 60% stake in a Saudi subsidiary and the purchase of a few naval units. (Company disclosure)

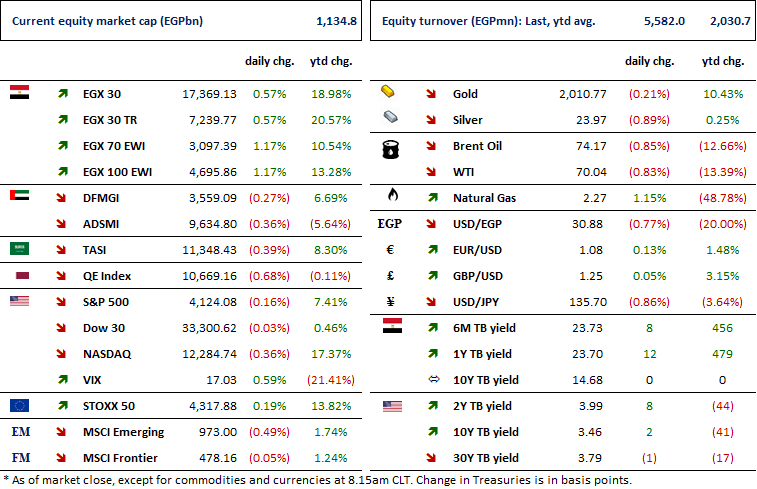

Markets Performance

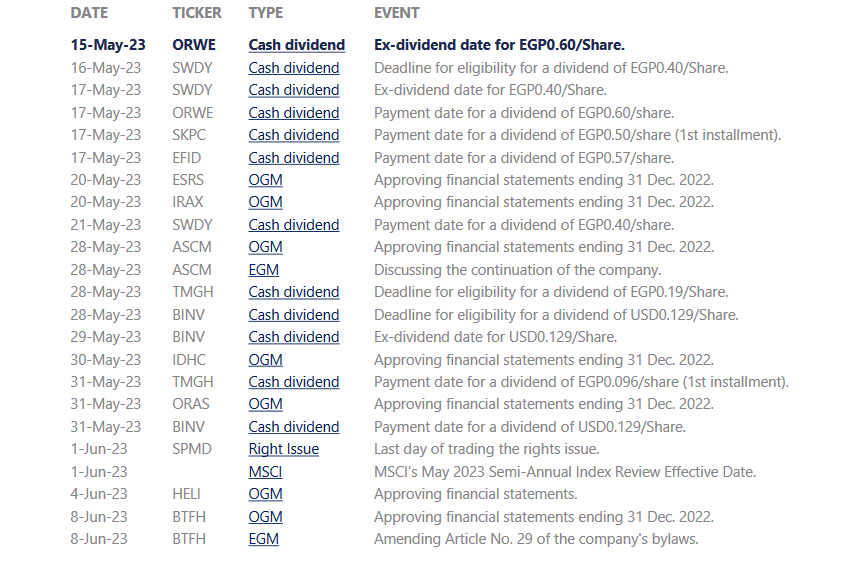

Key Dates

Latest Research