Today’s Top News & Analysis

CBE maintains key policy rates in its first meeting of the year

Egypt's BoP surplus jumps 68% y/y in Q1 FY23 on lower CAD and net errors & omissions

The energy sector will make up half of the companies offered on the EGX

A number of local banks reportedly resumed mortgage initiatives

GASC launches Russian wheat tender

Al Ezz Dekheila appointed as main supplier for El Daba’a Plant

EFG Hermes postpones the listing of ValU

MACRO

CBE maintains key policy rates in its first meeting of the year

The Monetary Policy Committee (MPC) decided in its first meeting of the year to maintain the overnight deposit rate, the overnight lending rate, and the rate of the main operation at 16.25%, 17.25 %, and 16.75%, respectively. The discount rate was also maintained at 16.75%.

Globally, the MPC said that forecasts for international commodity prices have marginally tightened, financial conditions continued to ease for the US economy, while the euro area’s financial conditions broadly stabilized.

Locally, the MPC stated that Egypt's real GDP growth recovered to 4.4% in Q3 2022 compared to 3.3% in Q2 2022, primarily driven by the improvement in tourism, agriculture and trade. However, the MPC decided to keep key policy rates unchanged in order to assess the impact of the implemented front-loaded tightening policies in a data-driven manner, having raised rates by a cumulative 8% in 2022, 5% of which in Q4 2022 alone.

On one hand, the future path of inflation is a function of the cumulative tightening in the monetary policy stance to date and the lag with which monetary policy tools operate. On the other hand, the path of future policy rates remains a function of forecasted inflation rather than prevailing inflation rates. The MPC noted that maintaining tight monetary conditions is a necessary condition to achieve the CBE’s inflation targets and price stability over the medium term. (CBE)

Egypt's BoP surplus jumps 68% y/y in Q1 FY23 on lower CAD and net errors & omissions

The Central Bank of Egypt (CBE) published Egypt's balance of payments (BoP) for Q1 FY23 ending 30 September 2022, registering an overall surplus of USD524mn compared to USD311mn in Q1 FY22. The current account deficit (CAD) improved by 20% y/y to USD3.2bn in Q1 FY23 compared to USD4bn in Q1 FY22, while the capital & financial account surplus fell 27% y/y to USD4.4bn compared to USD6bn in the comparable period. However, the y/y improvement was driven by lower net errors and omissions of a negative USD0.7bn from a negative USD1.7bn.

Below are our key takeaways:

· Trade deficit improved by 18% to USD9.1bn, as:

o Non-oil trade deficit improved by 18% y/y to USD9bn, driven by an increase in non-oil exports by 5% to USD6.3bn and a decline in non-oil imports by 10% to USD15.3bn.

o Oil trade deficit stabilizing at USD106mn, mainly due to:

§ A surge of USD807mn in oil exports on the back of a USD1.7bn increase in natural gas exports, despite a decline of USD450mn and USD393mn in crude oil exports and oil products, respectively.

§ An increase of USD812mn in oil imports.

· Tourism revenues increased by 43.5% y/y to USD4.1bn.

· Egyptians' remittances declined by 21% y/y to USD6.4bn.

· Investment income deficit rose 17% to USD4.5bn due to higher income payments for earnings on FDIs in Egypt and interest payments on external debt.

· Net foreign direct investments (FDIs) doubled y/y to USD3.3bn, driven mainly by:

o Net inflows of non-oil sectors on sale proceeds of companies to non-residents and net greenfield investments & capital increases of existing companies.

o Net outflows of the oil sector declining on the back of a rise in new investments of foreign oil companies and an increase in outflows from the exploration, development and operations previously incurred by foreign partners.

· Foreign portfolio investments (FPIs) registered a net outflow of USD2.2bn vs. an inflow of USD3.6bn a year before, on withdrawal of investments against the backdrop of the Russia-Ukraine conflict and a more hawkish U.S. Fed. (CBE)

CBE advises banks on the use of interbank USD proceeds

The CBE urged banks to strictly use USD proceeds from the interbank market to satisfy foreign currency importation needs by clients, not to cover deficits in foreign currency accounts. (Economy Plus)

The energy sector will make up half of the companies offered on the EGX

The Minister of Petroleum & Mineral Resources announced that up to half of the 20 companies expected to be offered on the EGX will belong to the oil and energy sector. The petroleum companies that could be included are Enppi, ELAB, and Wataneya. (Asharq Business)

A number of local banks reportedly resumed mortgage initiatives

A number of banks have reportedly resumed working with the CBE's mortgage initiatives at subsidized rates (i.e. 3% and 8%) after transferring the initiative under the Ministry of Housing & New Urban Communities. Sources added that namely National Bank of Egypt (NBE), Credit Agricole Egypt [CIEB], and Export Development Bank of Egypt [EXPA] have resumed the initiatives. (Economy Plus)

GASC launches Russian wheat tender

General Authority for Supply Commodities (GASC) signed a contract to purchase 535,000 tons of Russian wheat, financed by The World Bank. Shipments are set to arrive in the second half of February and the first half of March 2023. (GASC)

CORPORATE

Al Ezz Dekheila appointed as main supplier for El Daba’a Plant

The Nuclear Power Plants Authority appointed Al Ezz Dekheila Steel Co. (EZDK) [IRAX] as its main supplier of steel for El-Daba’a Nuclear Power Plant. EZDK is a 64%-owned subsidiary of Ezz Steel [ESRS]. Investments in El Daba’a Nuclear Power Plant are worth up to USD25bn. (Al-Mal)

EFG Hermes postpones the listing of ValU

EFG Hermes Holding [HRHO] postponed the listing of ValU, its consumer finance arm, on the EGX to be next year instead of this year. (Shorouk News )

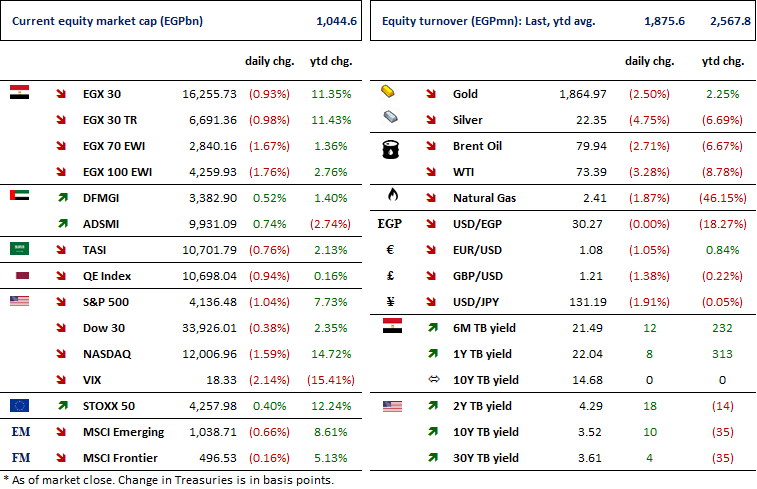

MARKETS PERFORMANCE

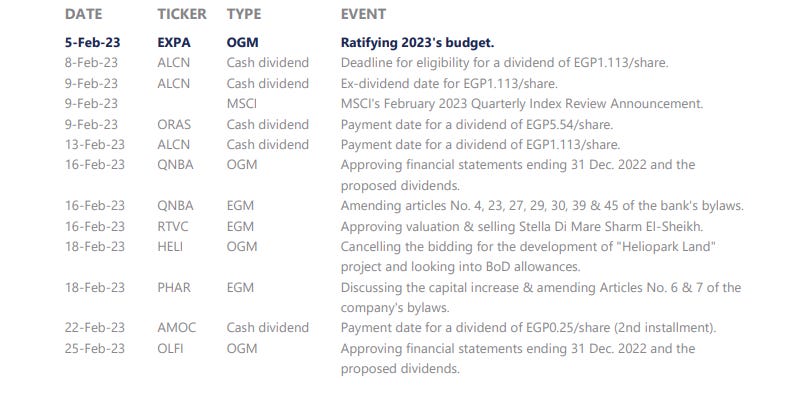

KEY DATES

Latest Research