Today’s Top News & Analysis

Reserve money (M0) increase to EGP1.56tn

Foreign investments in Egyptian treasuries increase to USD17.2bn in Q3 FY23

EKHO Q1 2023: Poor performance overshadows adequate sequential GPM growth

ORWE Q1 2023: Strong net profit growth

RMDA Q1 2023: Earnings slip y/y despite higher revenues

CIEB Q1 2023: Beyond expectations

SAUD Q1 2023: Relatively modest earnings

MOIL 2022: More net losses despite gross profits

KZPC Q1 2023: Triple-digit earnings growth

EGAS Q1 2023: Investment income and FX gains drive earnings growth

Amer Group to issue EGP1.5-2bn worth of Sukkok

MACRO

Reserve money (M0) increase to EGP1.56tn

The Central Bank of Egypt (CBE) reported that the reserve money increased to EGP1.56tn by the end of April 2023 vs. EGP1.50tn in March 2022. (Al-mal)

Foreign investments in Egyptian treasuries increase to USD17.2bn in Q3 FY23

Reportedly, foreign investments in the Egyptian treasuries increased to USD17.2bn in Q3 FY23. It is worth mentioning that this is the highest since March 2022 were it recorded USD17.5bn back then. (Al-mal)

Corporate

EKHO Q1 2023: Poor performance overshadows adequate sequential GPM growth

Egypt Kuwait Holding Co. [EKHO] released its Q1 2023 consolidated results, posting net income of USD60mn (-16% y/y, +77% q/q) on lower revenues of USD215mn (-22% y/y, -12% q/q) with a 46% GPM (-5pp y/y, +16pp q/q). The y/y lower earnings were driven by:

(1) Fertilizers (Alexfert) revenues declined by 38% y/y to USD77mn with a lower GPM of 41% (-17pp y/y), driven by:

· Lower local urea volumes of 37,400 tons (-14% y/y) at a lower selling price of USD152/ton (-50% y/y).

· Lower export ammonium sulphate volumes of 13,003 tons (-64% y/y) at a lower selling price of USD323/ton (-38% y/y).

· Lower selling prices across other products: Local ammonium sulphate of USD251/ton (-42% y/y) and exported urea of USD467/ton (-32% y/y).

· Not exporting any ammonia (only USD2.2mn in sales in Q1 2022).

(2) Drilling (ONS) revenues declined by 10% y/y to USD32mn with a lower GPM of 49% (-15pp y/y), driven by:

· Lower prices of USD5.7/MMSCFG (-3% y/y).

· Higher costs of USD2.3/MMSCFG (+32% y/y).

(3) Natural gas (Natgas) revenues declined by 35% y/y to USD20mn with a lower GPM of 31% (-14pp y/y), driven by:

· Fewer new installations for both household (19,581 clients, -43% y/y) and commercial (178 clients, -16% y/y) clients.

· Lower commission revenues of USD2.8mn (-38% y/y) due to lower prices.

(4) Lower investment and other income and higher interest expense.

Meanwhile, the company did improve in some areas:

(1) Chemical (Sprea) revenues improved 11% y/y to USD60mn with a higher GPM of 62% (+16pp y/y), driven by:

· Greater total sales volume of 1.48mn tons (+102% y/y) as a result of the capacity expansion for formica sheets, SNF, and sulfuric acid production lines.

· Lower total blended COGS/ton of USD15/ton (-63% y/y).

(2) Recording an FX gain of USD14mn in Q1 2023 vs. an FX loss of USD3.7mn in Q1 2022.

Furthermore, EKHO improved its margins from Q4 2022, which led the company to achieve a higher net income in Q1 2023 despite lower revenues q/q. This was achieved by:

· Alexfert’s lower total blended COGS/ton of USD216/ton (-21% q/q).

· Sprea’s lower total blended COGS/ton of USD15/ton (-68% q/q).

· An impairment reversal of USD0.1mn in Q1 2023 vs. an impairment loss of USD11mn in Q4 2022.

Lastly, the company outlined some of its expansion plans:

(1) Sprea: New powder SNF production line and adding capacity to the powder and liquid glue production lines.

(2) Nile Wood: Medium Density Fiberboard (MDF) production line is expected to begin in Q4 2023. (Company disclosure: 1, 2)

EKHO — Rating: OW / M, 12MPT: EGP56.8/share – USD1.9/share (29-Jan-2023)

ORWE Q1 2023: Strong net profit growth

Oriental Weavers Carpet [ORWE] reported Q1 2023 net profits of EGP411mn (+74% y/y) on high revenues of EGP4.1bn (+27% y/y). Similar to Q4 2022, ORWE's higher revenues were driven by higher selling prices, not volumes which dropped across the board to 27.4mn sqm (-22% y/y). As usual, the Egypt-based woven segment was the highest contributor to total revenues by 60% with EGP2.5bn (+21% y/y). Meanwhile, gross profit and EBITDA margins improved to 14% (+3pp y/y) and 15% (+4pp y/y), respectively. (Company disclosure)

RMDA Q1 2023: Earnings slip y/y despite higher revenues

Rameda [RMDA] reported Q1 2023 net profits of EGP67mn (-7% y/y) despite revenues growing by 14% y/y to EGP392mn. The decline in net profits can be attributable to three reasons:

(1) Lower gross profit margin of 46% (-5pp y/y) due to the higher costs because of the EGP devaluation.

(2) An impairment and provisions of EGP1.9mn (vs. EGP1mn a year before).

(3) One-off ESOP expenses of EGP4.5mn. (Company disclosure)

CIEB Q1 2023: Beyond expectations

Credit Agricole – Egypt [CIEB] announced the full standalone results for Q1 2023. Here are our main takeaways:

· Net income increased by 151% y/y to EGP1.2bn on the back of: (1) a 94% y/y increase in net interest income (NII) to EGP1.5bn. (2) reversal of provisions by EGP3mn. (3)188% y/y increase in net fees and commissions to EGP406mn. (4)109% y/y increase in net trading income to EGP153mn.

· The leap in NII pushed the annualized NIM up to reach 8.4%, while the record-breaking earnings pushed the annualized ROAE to 46%.

· The bank’s loan book growth came limited, by only 2.5% ytd to EGP36bn. Meanwhile, NPL ratio was maintained at 2.8% with a coverage ratio of 153%.

· Growth in deposits on the other hand came surprisingly strong by 12% ytd to EGP68bn, derived by corporate deposits. This caused the GLDR to decrease to 53%.

· Since the bank decided to distribute no cash dividends, CAR increased to 19.7%.

CIEB is currently traded at an annualized P/E of 4.5x, and a P/BV of 1.3x. (Bank disclosure)

SAUD Q1 2023: Relatively modest earnings

Al Baraka Bank – Egypt [SAUD] announced the full results for Q1 2023:

· Despite net interest income (NII) growing by 46% y/y to EGP1bn, net income growth came tamer at 20% y/y to EGP444mn.

· This was due to the following reasons: (1) 87% y/y higher provisions of EGP129mn. (2) 237% y/y higher other operating expenses of EGP32mn due to limited FX losses. (3) 35% higher administrative expenses of EGP301mn. (4) a leap in the effective tax rate to 38%.

· SAUD’s annualized NIM is still at 4.8%, the same as 2022. As for annualized ROAE, it dropped to 23% from 26% in 2022.

· On the balance sheet side, deposits came in flat at 1% ytd to EGP75bn.

· Instead, the bank resorted to the due to banks account to finance its assets growth. Accordingly, it increased by 249% ytd to EGP6.6bn.

· Loans grew by 7% ytd to EGP38bn, increasing the bank’s GLDR to 50%. NPL ratio came at 4.5% and coverage at 141%.

· Although the bank did not distribute any dividends for 2022, SAUD’s CAR continued to decline to 16% from 17.7% in 2022.

SAUD is currently traded at an annualized P/E of 3.4x and a P/BV of 0.8x. (Bank disclosure)

MOIL 2022: More net losses despite gross profits

Maridive & Oil Services [MOIL] released its preliminary 2022 consolidated results showing a 34% y/y increase in net losses to USD106mn on lower revenues of USD102mn (-12% y/y) with a 29% GPM (vs. a gross loss margin of 14% a year before). The company’s Q4 2022 results showed a 490% q/q increase in net losses to USD77mn on lower revenues of USD26mn (-13% q/q) and USD35mn in gross profits (vs. USD1.5mn in Q3 2022). Absent detailed financials, it seems that higher opex and non-operating items led to the wider losses. (Company disclosure)

KZPC Q1 2023: Triple-digit earnings growth

Kafr El Zayat Pesticides’ [KZPC] Q1 2023 net income came in at EGP100.3mn (+152% y/y), equivalent to 78% of 2022 net profits, on revenues of EGP448mn (+67% y/y). We believe the increase in revenues was powered by higher USD-linked selling prices of pesticides. Meanwhile, GPM improved to 31% (+6 pp y/y) on higher prices for pesticides. (Company disclosure)

EGAS Q1 2023: Investment income and FX gains drive earnings growth

Egypt Gas’ [EGAS] Q1 2023 results showed net profits improving by a 24% y/y to EGP93.8mn on revenues of EGP1bn (-19.5% y/y). The increase in Q1 2023 bottom line came mainly from a jump in investment income to EGP680.5mn (+36% y/y) and an FX gain of EGP29mn (+264% y/y). Meanwhile, EGAS recorded 45% y/y wider operating losses of EGP604mn. (Company disclosure)

Amer Group to issue EGP1.5-2bn worth of Sukkok

Amer Group Holding Co. [AMER] is looking to issue EGP1.5-2bn worth of Sukkok within the next two months. (Al-Borsa)

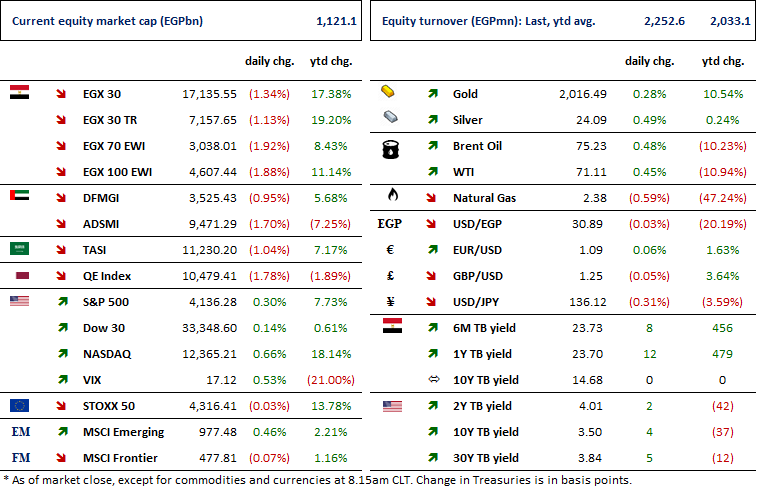

Markets Performance

Key Dates

Latest Research