Today’s Top News & Analysis

Fuel prices increased for the first time since last July

USD scarcity threatens another import crisis

The budget deficit target increases to 6.8% in FY23

NFAs are back to deterioration in January 2023

Egyptian bonds recorded the biggest losses among emerging markets

Egypt will deal in both EGP and USD in the sale of government assets

Egypt’s auto sales volumes hit the lowest since at least the start of 2018

Egypt to offer a new industrial city in the Administrative Capital

Egypt and Qatar studying to establish a joint investment fund

Elsewedy Electric 2022: Way above consensus

Lecico Egypt 2022: Back in the green

HELI 2022 (18M): 213% y/y increase in preliminary bottom line

HDBK 2022 preliminary: Record breaking earnings

ISPH 2022: Weak net profits with flat margins

POUL 2022 results: Higher revenues and net profits

RTVC Q3 2022: Higher net profits and wider GPM

EIPICO 2022: Strong earnings on higher revenues

SUGR BoD proposes cash dividends

Edita BoD proposes cash dividends

Macro

Fuel prices increased for the first time since last July

The Fuel Automatic Pricing Committee has released new increased fuel prices, driven by brent oil’s volatility and the FX rate. The new fees, effective today, are:

· EGP8.75/L (+9%) for octane-80 gasoline.

· EGP10.25/L (+11%) for octane-92 gasoline.

· EGP11.5/L (+7%) for octane-95 gasoline.

· EGP4.5/cubic m (+20%) for natural gas car fuel.

· EGP6000/ton (+20%) for industrial use mazut.

· EGP4600/ton (unchanged) for electricity generation and food industry mazut.

· EGP7.25/L (unchanged) for diesel fuel. (Ministry of Petroleum & Mineral Resources)

USD scarcity threatens another import crisis

Multiple banks have reportedly not received new letters of credit or collection documents from importers in the last two weeks, due to the persisting USD shortage. Banks have been reluctant to give out any foreign currency, as a result, some importers have faced delays in securing funds to release shipments from the ports. (Asharq Business)

The budget deficit target increases to 6.8% in FY23

The Egyptian Ministry of Finance raised its budget deficit target for FY23 to 6.8% of GDP (+70bps from the previous forecast). (Zawya)

NFAs are back to deterioration in January 2023

After two months of improvement, Net Foreign Assets (NFAs) for the Egyptian banking system declined by EGP160bn to reach negative EGP654bn in January 2023 against negative EGP494bn in December 2022. The reason behind the deterioration could be the external debt maturities and the import backlog clearing. (CBE)

Egyptian bonds recorded the biggest losses among emerging markets

Egyptian international bonds posted the biggest losses among emerging markets, with nine out of ten of the worst-performing bonds in the asset class belonging to Egypt. Bonds due in 2061 decreased by 3.6%, while bonds due in 2040 decreased by 2.9%. Credit default swap contracts, representing the cost of insurance against Egypt defaulting, increased to 1,052bps indicating investors’ fear of Egypt defaulting on its debt. (Asharq Business)

Egypt will deal in both EGP and USD in the sale of government assets

The government will value its assets in both EGP and USD terms when negotiating with investors; the choice of currency will be on a case-by-case basis. The decision will help reinforce investor appetites, especially after Saudi Arabia’s Public Investment Fund (PIF) halted its acquisition of The United Bank. (Asharq Business)

Egypt’s auto sales volumes hit the lowest since at least the start of 2018

Egypt’s auto sales volumes, according to Automotive Marketing Information Council (AMIC), declined to 5,400 vehicles in January 2022 (-75% y/y), hitting the lowest since at least the start of 2018 due to import restrictions and FX shortage as:

· Passenger car sales volume fell to 3,400 vehicles (-80% y/y).

· Truck sales volume fell to 1,140 vehicles (-62% y/y).

· Bus sales volume fell to 810 vehicles (-39% y/y). (Enterprise)

Egypt to offer a new industrial city in the Administrative Capital

The Administrative Capital for Urban Development is set to offer a 2000-acre industrial zone to investors in H2 2023. (Asharq Business)

Egypt and Qatar studying to establish a joint investment fund

The Egyptian Minister of Planning and Economic Development revealed that Egypt is studying with Qatar to establish a joint investment fund. (Asharq Business)

corporate

Elsewedy Electric 2022: Way above consensus

Elsewedy Electric's [SWDY] consolidated 2022 net profits came in at EGP5.4bn (+51% y/y) on revenues of EGP92.2bn (+52% y/y). Q4 2022 net profits registered EGP2.3bn (+79% y/y) on revenues of EGP29.6bn (+51% y/y). Both net profits and revenues came above our expectations by 38% and 10% and above market consensus by 25% and 7%, respectively. The revenue mix was as follows:

· The wires & cables segment recorded revenues of EGP43.7bn in 2022 (+47.5% y/y), contributing 46% of total sales, (+9% vs. our expectations). Q4 2022 revenues came in at EGP13.5bn (+44% y/y).

· The turnkey projects segment recorded revenues of EGP38.9bn in 2022 (+53.4% y/y), contributing 44% of total sales, (+11% vs. our expectations). Q4 2022 revenues came in at EGP12.9bn (+47% y/y).

· Turnkey projects backlog reached EGP85.8bn, with EGP2.4bn of new awards during Q4 2022 culminating into EGP38.6bn of awards for the whole year (-12% vs. our expectations).

· Other business segments recorded revenues of EGP9.1bn in 2022, contributing the remaining 10% of total sales, (+11% vs. our expectations). Q4 2022 revenues came in at EGP3.2bn (+111% y/y).

· EGP4.1bn from the Meters segments (+7% vs. our expectations).

· EGP3.7bn from the Transformers segments (+10% vs. our expectations).

A wider gross margin: GPM reached 14.7% (+0.7pp y/y, +1% vs. our expectations), supported by the increase in the wires & cables margins which reached 13.6% (+3pp y/y). By contrast, GPM for the turnkey segment decreased to 13% (-2pp y/y). Other electrical products and renewables segments maintained the highest margins with 48% and 54%, respectively.

Net interest expense increased to EGP1.2bn (+308% y/y), with the net debt reaching EGP15.1bn. The increase in debt was due to the company's decision to manage its inventory through stockpiling in an environment of rising commodity prices. This is apparent in the inventory’s DOH which increased from 93 days in 2021 to 112 days in 2022 (+11 days vs. our expectations), the highest in the last five years. This helped SWDY lessen the pressure on its margins during the year. Total debt amounted to EGP35.7bn (+87% y/y).

SWDY is one of the 15 stocks we picked in our STANDPoint 2023 strategy outlook published on 29 January 2023. (Company disclosure)

SWDY — Rating: OW / M, 12MPT: EGP21/share (29-Jan-2023)

Lecico Egypt 2022: Back in the green

Lecico Egypt [LCSW] consolidated statements for 2022 show a net profit of EGP12.7mn (above our expectations by c.50mn due to a higher USD/EGP during Q4 2022) compared to a net loss of EGP23.3mn during 2021. Revenues came in at EGP3.3bn (+23.9% y/y, +6.5% vs our expectations) while GPM stabilized at 18.3%. The revenue mix was as follows:

· Sanitary Ware segment sales contributed almost 61.3% of total sales with a total of EGP2bn (+24.6% y/y). Volumes slightly increased by 2%, while the average price per piece for the segment increased by 22% to reach EGP392.8/piece, powered by the weakening EGP. GPM for the segment decreased by 1.4pp y/y to 12.7%. Exports contributed 72.8% of total sales for the Sanitary Ware segment.

· Tile segment sales contributed 32.8% of total sales with a total of EGP1.1bn (+21% y/y). The increase in tile sales is attributable to a 5% increase in volumes sold and an increase in the average price per piece for the segment by 15% to reach EGP48.2/sqm. GPM for the segment increased by 1.6pp y/y to 24.2%.

· Brassware segment contributed the remaining 5.9% of total sales with a total of EGP185.7mn (+34% y/y). The increase in Brassware sales is attributable to a 16% increase in volumes sold and the increase in average price/piece by 15% to reach EGP1067.7/piece. The GPM for the Brassware segment is still the highest among LCSW's business segments, with a GPM of 44.6% (+5.3 pp y/y).

· Finance income reached EGP317mn, including an EGP312mn in FX gains. On the other hand, financing expenses remained high at EGP209.3mn (+167% y/y). The increase in financing expense is due to the rising interest rate environment, an EGP104.2mn loss on future contracts, and the increase in LCSW's total debt, which reached EGP1.4bn in 2022. (Company disclosure)

LCSW — Rating: UW / H, 12MPT: EGP4.3/share (19-Oct-2022)

HELI 2022 (18M): 213% y/y increase in preliminary bottom line

Heliopolis Company for Housing and Development [HELI] 2022 (18M) preliminary results show net profits of EGP652.7mn (+213% y/y) on revenues of EGP2bn (+128% y/y). GPM came at 60% (+14.5pp y/y). (Company disclosure)

HDBK 2022 preliminary: Record breaking earnings

Housing & Development Bank [HDBK] announced exceptional preliminary results for 2022.

· The bank's net income increased by 23% y/y to EGP2.2bn reaching a new peak. This was mainly on the back of a 50% increase in net interest income to EGP4.9bn.

· HDBK’s loan book grew by 42% y/y to EGP38bn, with major improvement in NPL ratio at 7% down from 10% last year. As for Coverage ratio, as the bank booked 3x higher provisions at EGP645mn, it increased to 109% up from 83%.

· As for deposits, HDBK recorded the highest deposits growth in the market by 42% y/y to EGP89bn, pushed by corporate/low-cost CASA deposits. Now the GLDR ratio stands at 43%.

· HDBK’s ROAE INCREASED BY 3 PPS TO 23%, while NIM stood at 6.7%.

· BoD has suggested distributing dividends of EGP1/share, which implies a payout ratio of 24% and a dividends yield of 4.6%.

· The bank is currently traded at a PE of 5.2x and a PB of 0.9x. (Bank disclosure)

ISPH 2022: Weak net profits with flat margins

Ibnsina Pharma [ISPH] reported 2022 net profits of EGP173mn (-45% y/y) with revenues of c.EGP22bn (+2% y/y). Net profits decreased due to:

· Higher credit risk resulting in provisions of expected claims of EGP65mn.

· Interest expense increased to EGP477mn (+68% y/y).

Meanwhile, gross profit margin came in flat at 7.3% (-0.2% y/y).

Despite the y/y decline in net profits, Q4 2022 posted better q/q results:

· Net profits of EGP53mn (+71% q/q).

· Revenues of EGP6.5bn (+16% q/q).

Gross profit margin declined by 1.2pp q/q to 6.5%. (Company disclosure)

POUL 2022 results: Higher revenues and net profits

Cairo Poultry Company [POUL] reported 2022 net profits of EGP296mn (+62% y/y), on higher revenues of EGP6.5bn (+30% y/y) due to higher selling prices across all products. The increase in selling prices came due to:

· High commodity prices due to the Russia Ukraine war.

· USD shortage due to the higher FX rates.

Meanwhile, gross profit margin improved by 1pp y/y to 13%.

Regarding Q4 2022, net profits grew to EGP76mn (+26% y/y), compared to net losses of EGP16mn in Q3 2022. The increase in net profits came in due to:

· Higher revenues of EGP1.8bn (+31% y/y), (+7% q/q).

· Lower tax expenses of EGP38mn compared to EGP96mn in Q3 2022. Where POUL noted that the high tax expenses in Q3 2022 was the reason behind posting net losses rather than profits.

· Whereas, gross profit margin came in flat at 13% (-0.5pp y/y) and expanded by 5pp q/q.

On a separate note, POUL intends to invest EGP150mn during the year to develop the company’s existing assets and increase investment in the process of marketing the company’s products. (Company disclosure, Al-Mal)

RTVC Q3 2022: Higher net profits and wider GPM

Remco Tourism Villages Construction [RTVC] reported consolidated Q3 2022 net profits of EGP73mn compared to a net loss of EGP69mn in Q3 2021, on higher revenues of EGP150mn (+53% y/y). GPM expanded by 16pp y/y to 54%. (Company disclosure)

EIPICO 2022: Strong earnings on higher revenues

EIPICO [PHAR] reported its consolidated 2022 net profits of EGP643mn (+32% y/y) on higher revenues of c.EGP4.0bn (+15% y/y). Local sales contribution was 75% at c.EGP3.0bn (+11% y/y), representing 2.5% of total pharma sales in Egypt (EGP118tn). Whereas GPM slipped by 2pp y/y to 42%. Regarding Q4 2022, net profits grew to EGP226mn (+38% y/y), (+208% q/q) due to the following:

· Higher revenues of EGP1.3bn (+25% y/y), (+33% q/q).

· FX gains of EGP186mn compared to EGP22mn in Q3 2022.

· However, GPM declined to 37% (-11pp y/y), (-6pp q/q). (Company disclosure)

SUGR BoD proposes cash dividends

Delta Sugar [SUGR] BoD proposed distributing cash dividends with a total of EGP363mn (EGP2.5/share), to be paid in two tranches:

· 5% of the paid-in capital as primary cash dividends, amounting to EGP36mn.

· 46% of the paid-in capital as bonus cash dividends, amounting to EGP327mn. (Company disclosure)

Edita BoD proposes cash dividends

Edita Food Industries [EFID] BoD proposed distributing EGP0.553/share cash dividends, implying a 3% yield. (Company disclosure)

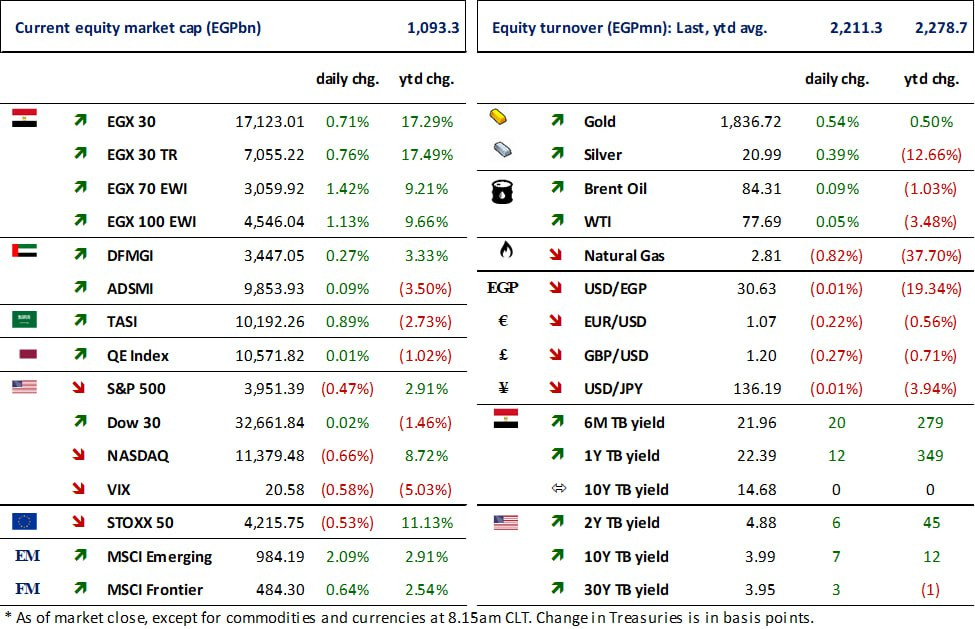

Markets Performance

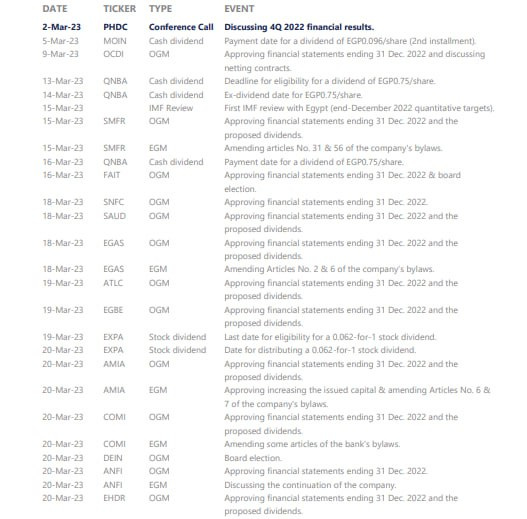

Key Dates

Latest Research