Today’s Top News & Analysis

EIB could invest in water projects in Egypt

State Ownership Policy is expected this year

Telecom Egypt reports Q3 2022 results; Vodacom to buy a marginal minority stake in VODE

CIEB’s Q3 2022 preliminary results show strong balance sheet growth

ADIB announces another operationally strong quarterly earnings

EGBE reports full Q3 2022 financials

Oriental Weavers announced its Q3 2022 results

PACHIN reports 2021/22 and Q1 2022/23 results

MM Group discloses Q3 2022 results

Raya Contact Center announced its Q3 2022 results

Misr Cement Qena reports Q3 2022 results

Misr Beni Suef Cement reports Q3 2022 results

Sinai Cement reports 9M 2022 results

Ibnsina Pharma announced its Q3 2022 results

EK Holding saw 36% y/y earnings growth

A consortium to build one of the largest wind farms in the world in Egypt

MACRO

EIB could invest in water projects in Egypt

The European Investment Bank (EIB) plans to commit USD1.5bn in new financing to Egypt, primarily focusing on water treatment. (Enterprise)

State Ownership Policy is expected this year

The Egyptian government’s State Ownership Policy document could go into effect at the end of this year. (Enterprise)

CORPORATE

Telecom Egypt reports Q3 2022 results; Vodacom to buy a marginal minority stake in VODE

Telecom Egypt [ETEL] reports its Q3 2022 results, where net income grew 7% y/y to EGP2.4bn despite 32% y/y higher revenues of EGP11.9bn. Adjusted for provisions and FX impact, Q3 2022 net income would have grown by 40% y/y. Around 55% of revenue growth came from cable projects due to the recognition of the EGP1.6bn Sea-Me-We 6 subsea cable. EBITDA grew 47% y/y, implying an EBITDA margin of 44%. Customer numbers rose across the board (fixed voice +8% y/y, fixed data +12% y/y, and mobile +54% y/y). Meanwhile, Vodacom has submitted an offer to buy a 0.05% stake in Vodafone Egypt [VODE] or 124,608 shares for EUR17.92/share for a total value of only EUR2.2mn. The disclosure suggests that Vodacom had extended a similar offer to Telecom Egypt [ETEL] for its stake in VODE, which ETEL declined. The abovementioned offer is a marginal minority stake in VODE, which should not be relied on in valuing VODE, in our opinion. (EGX, Company disclosures: 1, 2)

CIEB’s Q3 2022 preliminary results show strong balance sheet growth

Credit Agricole – Egypt’s [CIEB] Q3 2022 preliminary standalone results showed the following:

· A 14% q/q increase in net interest income to EGP968mn (+32% y/y).

· However, net income decreased 19% q/q to EGP586mn (+45% y/y).

· CIEB’s balance sheet demonstrated significant growth in both loan book (+10% q/q, +13% ytd) to EGP35bn and deposits (+9% q/q, +11% ytd) to EGP54bn. Indeed, this quarter alone represents almost all ytd growth in CIEB’s balance sheet. (Company disclosure)

ADIB announces another operationally strong quarterly earnings

· Net income showed a modest 4% q/q increase to EGP570mn (+58% y/y), although net interest income (NII) for the quarter increased 12% q/q to EGP1.3bn (+40% y/y).

· This can be attributed to other operating expenses of EGP126mn due to booking other contingent provisions against other operating income of EGP6mn last quarter. These provisions have offset the effect of FX gains of the quarter.

· Strong NII performance was fueled by 7% q/q growth in ADIB’s loan book to EGP55bn (+21% ytd), with a 3bps lower NPL ratio of 2.2% and a 14bps higher coverage ratio of 179%.

· The provisioning rate for ADIB remained almost the same q/q as it booked 15% q/q lower provisions of EGP150mn, decreasing its annualized CoR to -1.08%.

· Deposits recorded a 4% q/q increase to EGP86bn (+13% ytd) with a higher GLDR of 67%.

· It is also notable that ADIB grew its interbank assets by 82% q/q to EGP10.4bn (+123% ytd) in response to the latest high yield OMOs by the CBE.

· ADIB’s annualized NIM increased to 5.6%, while the annualized ROE is now at 26%.

· ADIB is now traded at an annualized P/E of 2.2x and a P/BV of 0.6x. (Company disclosure)

EGBE reports full Q3 2022 financials

Egyptian Gulf Bank [EGBE] announced its full standalone results for Q3 2022:

· Although net interest income (NII) increased strongly by 17% q/q to EGP800mn (+10% y/y), this increase did not filter through to the bottom line which remained almost flat q/q at EGP215mn (+24% y/y).

· This was on the back of many factors, one of which is the 360% q/q higher booked provisions of EGP113mn (+99% y/y). The other factors were the 53% lower other operating income of EGP9mn and a 300bps higher effective tax rate (ETR) of 47% against 44% last quarter.

· EGBE managed to pick up loan growth with a 2% q/q increase to EGP25.6bn after it declined last quarter. This raises its loan book ytd growth to 10%, while maintaining the same NPL ratio of 4.5% and coverage ratio of 117%.

· EGBE’s deposits continue to grow steadily by 4% q/q to EGP74bn (+14% ytd), suggesting a GLDR of 37%. This low GLDR is due to the increasing investments in debt securities that increased 104% q/q to EGP10bn to benefit from the high sovereign yields, which explains the higher ETR mentioned above.

· EGBE’S annualized NIM is now at 4%, while annualized ROE stands at 17%.

· EGBE is now traded at an annualized P/E of 7x and a P/BV of 0.9x. (Company disclosure)

Oriental Weavers announced its Q3 2022 results

Oriental Weavers Carpet [ORWE] reported a consolidated net profit of EGP79mn (-69% y/y) in Q3 2022 despite higher revenues of EGP3.0bn (+7% y/y) as gross profit margin decreased to 8.5% (down 7pp y/y). Also, ORWE booked in Q3 2022 expected credit losses of EGP24mn and provisions of EGP32mn as well as 18% higher y/y general and admin expenses and 69% higher y/y higher interest expense. (Company disclosure)

PACHIN reports 2021/22 and Q1 2022/23 results

Paints & Chemical Industries’ (PACHIN) [PACH] consolidated 2021/22 results show a net loss of EGP0.4mn compared to a net profit of EGP52.7mn a year before. Revenues came in at EGP860mn compared to EGP850mn in 2020/21 (+1% y/y). The loss is mainly attributable to higher costs, where GPM came in at 9.8% (-8.5 pp y/y). PACH also announced its Q1 2022/23 preliminary results, where earnings before taxes came in at EGP10.3mn compared to EGP2.7mn a year before. Revenues reached EGP225.5mn compared to EGP213.3mn (+5.7% y/y), while GPM increased to 15.7% (+4.8 pp y/y), implying an improvement of PACH's margins back to their historical levels. In other news, PACH’s BoD agreed for National Paints LTD. to start due diligence to acquire 100% of the company for EGP29/share. (Company disclosures: 1, 2)

MM Group discloses Q3 2022 results

MM Group for Industry [MTIE] released its Q3 2022 results, where net earnings fell by 16% y/y to EGP72.3mn. This was due to the decrease in operating revenues by 35% y/y to EGP1.5bn. (Company disclosure)

Raya Contact Center announced its Q3 2022 results

Raya Contact Center [RACC] reported a consolidated Q3 2022 net loss of EGP6mn compared to a net profit of EGP10mn a year before despite 66% y/y higher revenues of EGP307mn. (Company disclosure)

Misr Cement Qena reports Q3 2022 results

Misr Cement Qena [MCQE] Q3 2022 results show net profits coming in at EGP10mn (-78% y/y), an improvement over the last quarter's net loss of EGP6mn. Revenues reached EGP673mn (+10% y/y) despite sales volumes decreasing to 591k tons compared to 849k tons in Q3 2021 (-30% y/y). GPM came in at 9% in Q3 2022 compared to 22% in the same period last year. The drop in GPM is attributable to the inflationary commodity prices environment and the FX fluctuations, which pressured MCQE's margins during the quarter. MCQE's Ready Mix Concrete segment sales increased by 8% y/y to EGP77mn during the quarter, while sales volume decreased by 20% y/y to reach 78k cubic meters. (Company disclosure)

Misr Beni Suef Cement reports Q3 2022 results

Misr Beni Suef Cement [MBSC] announced its Q3 2022 results, where its bottom line turned into a loss of EGP52.4mn compared to the same period last year's profits of EGP3.5mn. Revenues reached EGP530.4mn (+100% y/y), which is mainly due to an increase in sales volumes and the higher cement price compared to Q3 2021. Gross loss margin reached 11.8% compared to 5.6% in Q3 2021 (-6.2pp y/y). (Company disclosure)

Sinai Cement reports 9M 2022 results

Sinai Cement [SCEM] announced its 9M 2022 results, where the company's bottom line is still in the negative territory with a net loss EGP176.7mn compared to a net loss of EGP323.3mn in 9M 2021. Revenues reached EGP1.6bn (+64% y/y), mainly due to the higher cement prices, while sales volume growth flattened y/y. GPM came in at 6.4% compared to a GLM of -3.5% in the same period last year. (Company disclosures: 1, 2)

Ibnsina Pharma announced its Q3 2022 results

Ibnsina Pharma [ISPH] reported consolidated net profits of EGP31mn (-78% y/y) in Q3 2022 as revenues fell to EGP5.6bn (-1.4% y/y) and gross profit margin and EBITDA margin decreased to 7.7% (-1.1pp y/y) and 3.8% (-1.5pp y/y), respectively. (Company disclosure)

EK Holding saw 36% y/y earnings growth

EK Holding [EKHO] reported Q3 2022 results, with a strong 36% increase in attributable bottom line to USD64mn (-12% q/q) on the back of both revenue growth and substantial margin improvement. EKHO’s consolidated revenues grew to USD273mn (+29% y/y), with strong growth contribution coming from the fertilizers & petrochemicals segment on surging global prices. On the other hand, the energy & energy-related segment top line slowed due to a halt in production at ONS in view of an operational incident that has since been resolved. As a result, EBITDA margin for EKHO in Q3 2022 recorded 49% (+3pp y/y). EKHO is currently traded at 2022e P/E of 5x. (Company disclosure)

A consortium to build one of the largest wind farms in the world in Egypt

A Masdar-Infinity-Hassan Allam consortium could sign the contracts for a 10GW wind farm in southern Egypt by the end of the year. The wind farm is set to be one of the largest in the world. (Enterprise)

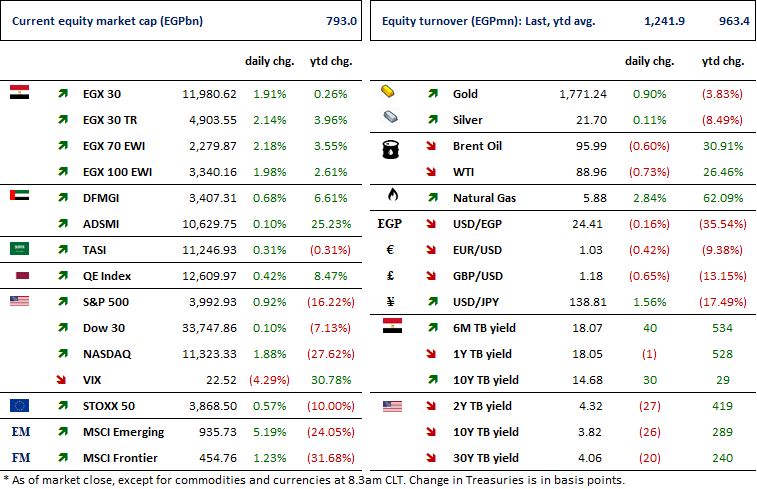

MARKETS PERFORMANCE

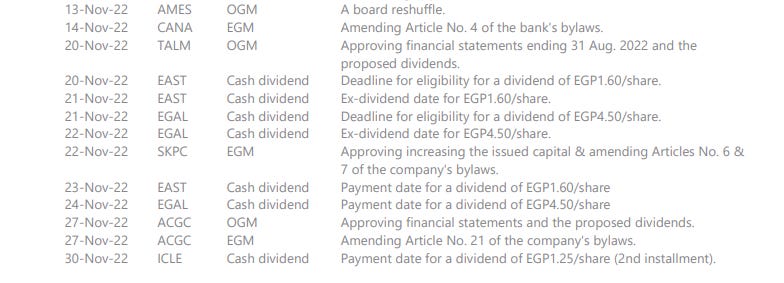

KEY DATES

Latest Research